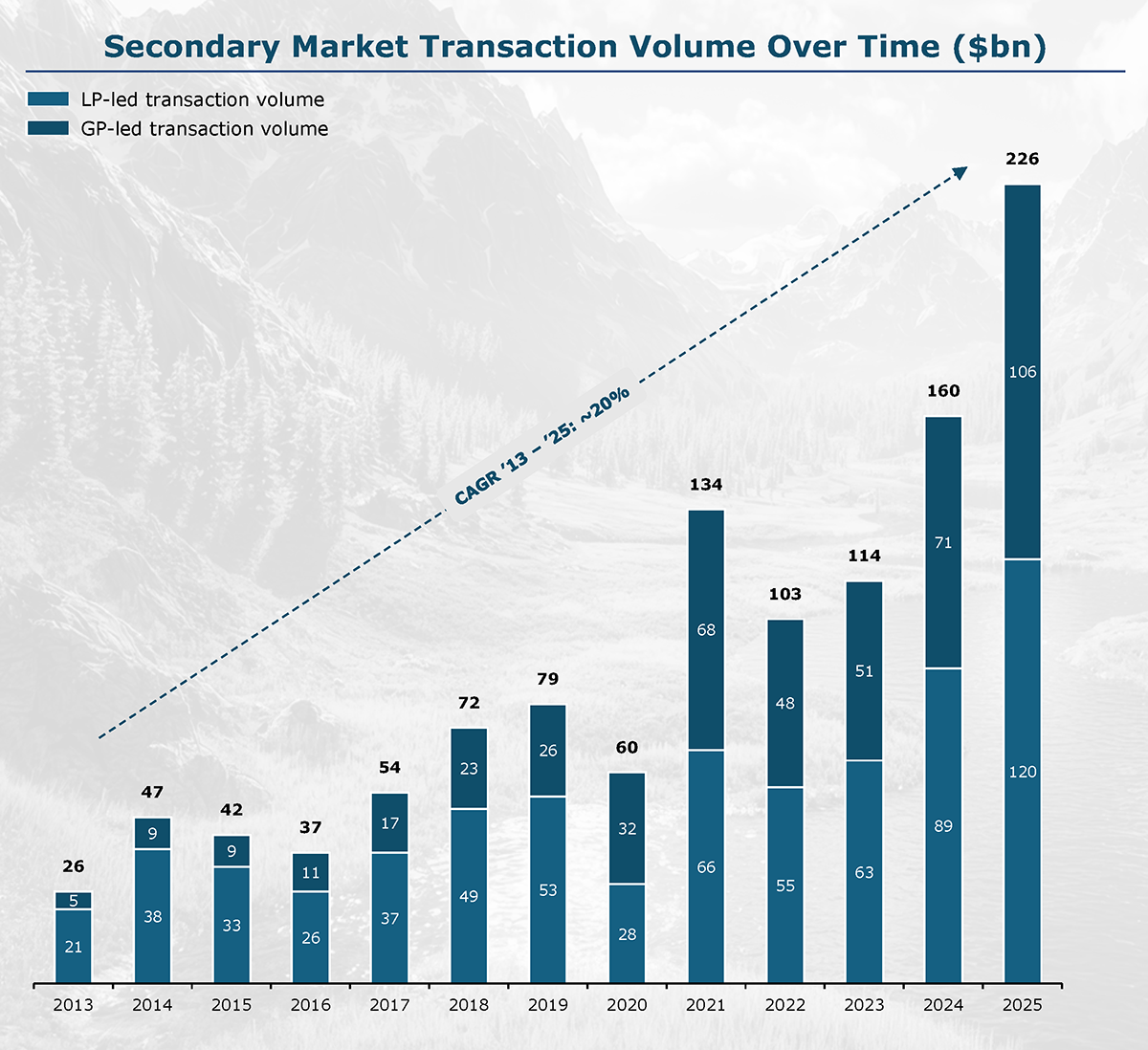

The secondaries market for limited partner stakes in private funds rose to a record $226 billion in 2025, according to a report from Evercore Inc.’s Private Capital Advisory group. The 41% increase from the prior year comes as investors embrace the marketplace as a tool for portfolio optimization.

Limited partner-led volume—in which institutional allocators sell their stakes in private funds on the market, often at a discount—rose 34% year-over-year to $120 billion, according to Evercore. The general partner-led secondary market—in which GPs extend the life of their funds through continuation vehicles and evergreen structures—rose 51% to $106 billion.

In comparison, the secondaries market stood at only $26 billion in 2013. The market surged during and after the COVID-19 pandemic: Volume stood at $60 billion in 2020 and more than doubled to $134 billion the following year.

Source: Evercore Private Capital Advisory

Full-year volume in 2025 far exceeded Evercore’s original end-of-year predictions of $171 billion in total volume—$97 billion in the LP-led market and $74 billion in the GP-led market.

The secondaries market grew as private equity firms were slow to exit their investments and return capital to their LPs. The average length of private funds also continued to increase. LPs were continuing to embrace the secondaries market as a tool for managing liquidity, rather than selling underperforming fund stakes out of desperation.

The Evercore report noted that LPs were supported by strong pricing of secondary fund sales. The discounts that private fund stakes were being sold at continued to decline—a report from CAIS noted that buyout private equity stakes were being sold at 94% of net asset value in the first half of 2025, compared with less than 90% in 2022.

“The increase in volume took place amid a still-high-interest rate environment,” says Michael Bego, managing partner in Kline Hill Partners. “This could imply a potentially weaker vintage for 2025 secondary deal-making, unless 2026 comes to the rescue with the unleashing of long-awaited liquidity, especially if it comes with strong appreciation.”

Private equity continued to make up a majority of secondary market volume, with 81% of all LP-led transactions and 77% of all GP-led volume. Evercore noted that the private credit secondaries market—7% of all LP-led and 11% of all GP-led volume—also reached record highs. Niche secondaries strategies, such as venture capital, infrastructure and other alternative asset classes, continued to gain interest.

“Venture volume has finally picked up as we are now getting far enough along past the 2021 tech bubble for valuations,” Bego says. “More importantly, there’s renewed confidence in tech companies and their business models. Valuations are finally returning to a more balanced state.”

Last year saw several notable secondaries transactions, including the Harvard University endowment selling a $1 billion stake, as well as the New York City pension system’s $5 billion private fund stake sale to Blackstone.

Related Stories:

Coller Capital, Ares Management Raise Billions for Secondaries Funds

Secondaries, and Market Complexity, on the Rise

LP-, GP-Led Secondaries Grow to Record Volumes in 2025

Tags: Evercore, Private Equity, secondaries