The surge in demand for data centers and the energy sources to power them has created a multi trillion-dollar opportunity for institutional investors.

The surge in demand for data centers and the energy sources to power them has created a multi trillion-dollar opportunity for institutional investors.

Hyperscalers—the large-scale providers of computing power—have committed hundreds of billions of dollars to different sectors of digital infrastructure in order to support the artificial intelligence boom. OpenAI’s Project Stargate zealously aims to invest more than $500 billion in such projects. Meta Platforms forecasts it will spend up to $72 billion in capital this year on data centers, while Microsoft has said it plans to spend $80 billion this year.

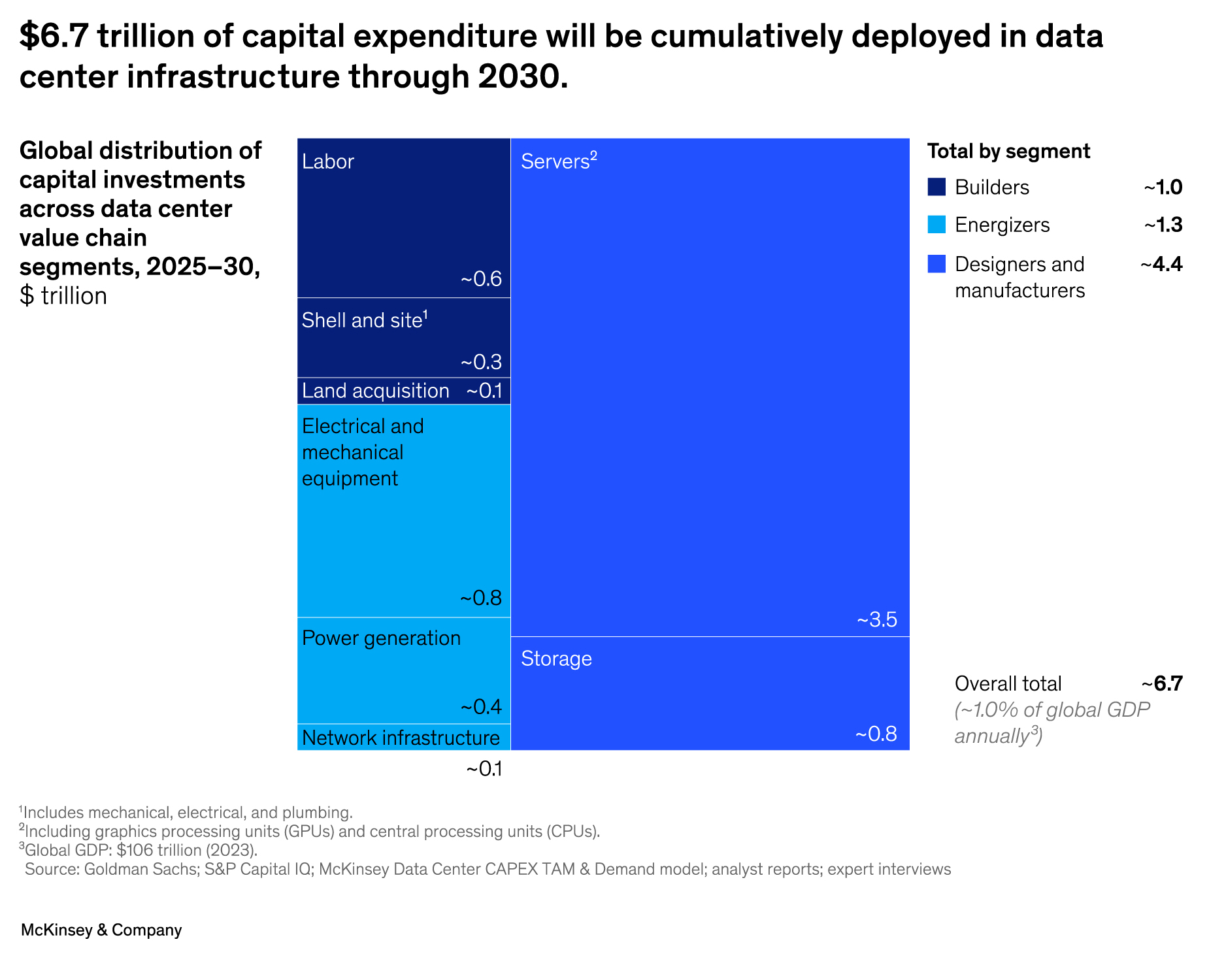

In total, the largest hyperscalers are estimated to spend $300 billion on data centers this year, Blue Owl Capital’s head of digital infrastructure Matt A’Hearn wrote in April. By the end of the decade, McKinsey & Co. estimates $7 trillion will be spent in total across the digital infrastructure ecosystem, a figure that includes $5.2 trillion estimated as needed for data centers alone.

Asset managers who specialize in infrastructure investing and private debt financing are capitalizing on the demand for both data centers and the energy sources needed to power them. Asset owners can gain exposure in the private markets through a number of asset classes, from real assets and infrastructure to private credit and venture capital.

Meta selected Blue Owl Capital and PIMCO in August for $29 billion in financing for a data center project in Louisiana. Nuveen, in August, raised $1.3 billion for an energy and power infrastructure credit fund. In April, PGIM Real Estate raised $2 billion for the final close of its Global Data Center Fund.

“We continue to see significant and growing demand from LPs to gain exposure to data centers. Institutional investors increasingly want to allocate to this sector because it sits at the intersection of two powerful long-term trends, digitalization and infrastructure,” says Erwin Thompson, partner in EQT Group, which owns data center provider EdgeConneX.

“Data centers form the mission-critical backbone for cloud computing, AI, and the broader digital economy, combining an infrastructure risk profile from long-term, high quality cash flow with meaningful opportunities for growth and value creation,” Thompson says.

Micah Bible, partner at Deloitte & Touche LLP, notes that institutional investors are primarily investing in digital infrastructure through allocations to private real estate and infrastructure funds. “The PE Infrastructure product has been a magnet for capital over the last 5 years as many investors seek to balance their portfolios with longer duration, inflation resistant, stable yields,” Bible says. “However, we also frequently see large pension funds and sovereign wealth funds pursuing direct investments in Infra projects, including data centers. Co-investment platforms allow for greater access and alignment of risk/return profiles.”

According to Nuveen’s 2025 EQuillibrium Global Institutional Investor Survey, 65% of surveyed asset owners said they planned to increase their allocations to digital infrastructure-focused real estate.

“Investors are increasingly interested in strategies that capitalize on their conviction in the growing global energy demand brought on by digitalization, electrification and reindustrialization while also seeking downside risk mitigation to guard against macro volatility, and inflationary and geopolitical risk,” said Don Dimitrievich, senior managing director and portfolio manager of energy infrastructure credit at Nuveen in a statement.

The number of specialist managers who focus on digital infrastructure has significantly increased over the last decade. According to a 2023 paper from Meketa, there were less than four digital infra managers in the market every year between 2012 and 2020. For the 2021 to 2023 vintage years, there were 36 such offerings from digital infrastructure managers.

“Manager selection becomes increasingly essential to navigating the new offerings and emerging firms formed to take advantage of the market demand,” the Meketa paper states.

According to CBRE’s upcoming North America Data Center Trends H1 2025 report, data center vacancy rates in North America hit an all-time low of 1.6%, driven by the demand from hyperscalers for AI capacity—demand for data centers is outpacing supply in every market, which in turn has elevated lease costs, with “intense” competition for available power and infrastructure resources.

As hundreds of billions, if not trillions of dollars are set to be invested in digital infrastructure over the decade, questions have been raised about the profitability of many large language models, but no hyperscale wants to be left behind in the AI race.

“The risk of under-investing is dramatically greater than the risk of over-investing,” Google CEO Sundar Pichai said last July.

Energy Requirements Compound

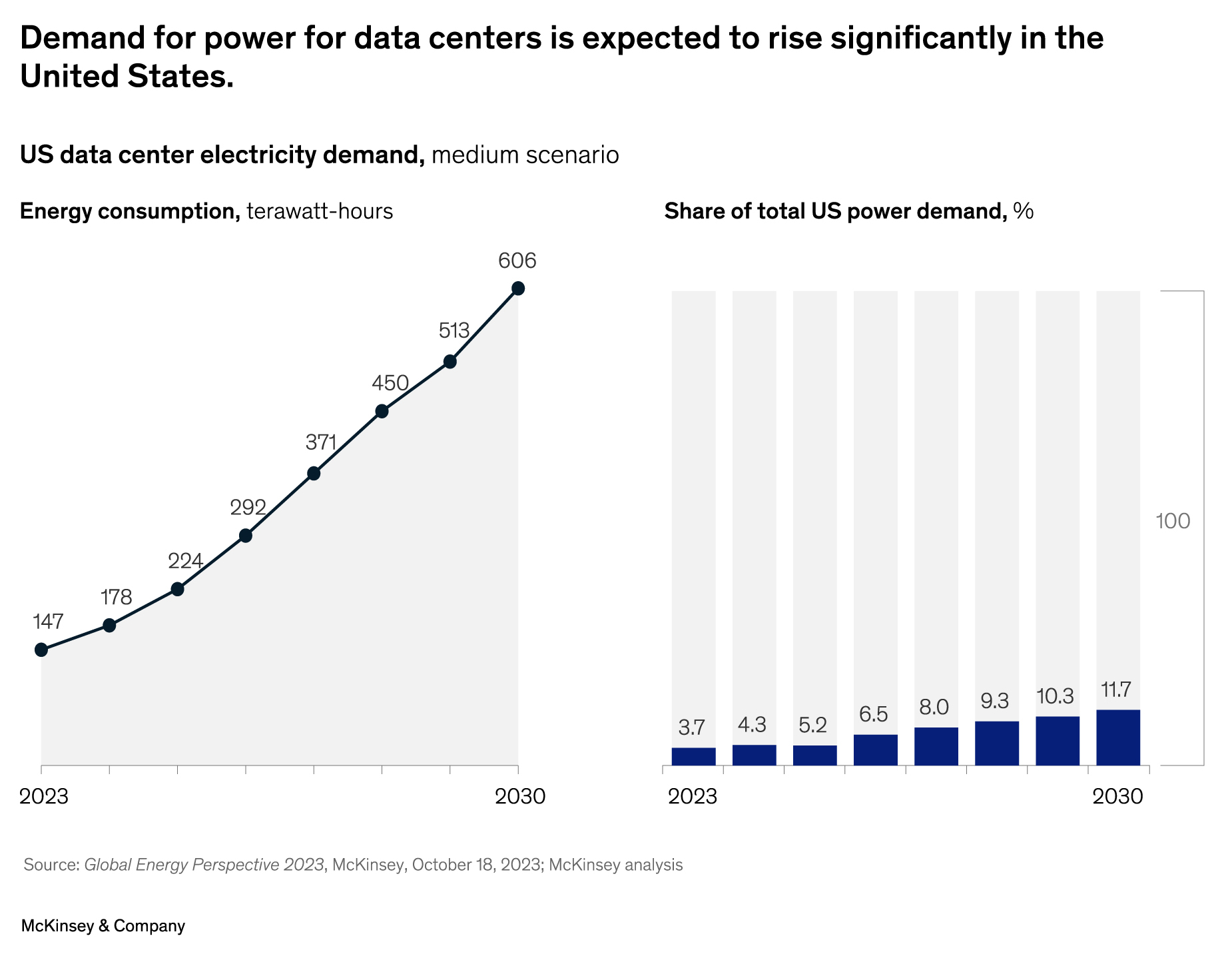

Power demand from data centers is expected to grow 50% by 2027 and 165% by the end of the decade, according to research from Goldman Sachs. This demand for power could require $720 billion in grid spending by 2030, the bank projected.

“Access to large-scale power generation is one of the most important enablers of future data center growth and represents one of the largest investment opportunities in the sector today,” Thompson says.

“Energy and power infrastructure face substantial challenges in keeping up with this demand, including grid capacity constraints, supply chain disruptions, and long permitting processes,” says Martin Stansbury, principal at Deloitte & Touche LLP. “Collaboration across industries and innovation in technology and regulatory frameworks will be crucial to address these gaps and support the evolving infrastructure needs.”

In the firm’s 2025 Infrastructure Market Overview, Hamilton Lane notes that power markets in the U.S. are facing both decreasing supply and increasing demand, which has led to substantial load growth for the first time in a decade, with one of the primary demand drivers being data centers for AI.

“Keeping up the pace of adding new generation to support data center buildout is a challenge no matter what energy resource you’re talking about,” says David Boyce, CEO, North America of Schroders Greencoat, a specialist manager dedicated to the renewable energy infrastructure sector.

The need for multiple sources of power could also clash with managers’ and asset owners’ pledges to achieve net zero emissions portfolios, as most energy sources, including both renewable and non-renewable power plants are not able to scale as quickly as needed to meet the power demands from data centers.

“At the scale and speed required for current AI workloads, there’s no fully sustainable substitute,” says Joel Slater, director at Stax Consulting. “Large scale renewables paired with grid-scale storage are the long-term goal, but they take years to permit and build. In the near term, efficiency gains, demand management, and cleaner grid power contracts can help reduce the carbon footprint while bridging to more sustainable capacity.”

In the meantime, Slater notes, the demand for gas-powered data centers has surged, as natural gas is able to scale much faster than other energy sources to meet the power demand. According to the U.S. Energy Information Administration, record natural gas consumption is expected in 2025.

Hyperscalers have turned to emerging power sources, like small modular nuclear reactors from startups backed by venture capital, and even fusion energy, to help meet the energy demand from their data centers.

Google’s partnership with startup nuclear energy company Kairos Power is one such agreement, as is Amazon’s partnership with independent power producer and energy infrastructure company Talon Energy. Microsoft, in 2023, signed a power purchase agreement to buy fusion power from Sam Altman-backed Helion Energy, sometime in 2028.

These projects are still years out. “You can’t just snap your fingers and [say] I want to buy a piece of land and tomorrow start building one of these things,” Boyce says. “It will take multiple years to develop them… there is a still, perceived at least, a large risk around cost to install and operating costs. And until those become better known, it’s hard for developers, private companies, anyone, it’s very difficult to take that bet.”

Regulatory, Other Hurdles Grow

Permitting is often a bottleneck for getting infrastructure and power projects off the ground and built—approvals for transmission lines and other energy infrastructure projects often take years, sometimes taking longer than the actual construction of a project.

“In both the U.S. and the EU, it usually takes longer to permit infrastructure projects than to construct them,” BlackRock chairman and CEO Larry Fink wrote in his 2025 annual letter. “A high-voltage power line can take 13 years to get approved—something China does in a quarter of the time.”

These hurdles have constrained data center supply, according to Goldman Sachs.

“Data center supply — specifically the rate at which incremental supply is built — has been constrained over the past 18 months,” wrote Goldman Sachs digital infrastructure analyst James Schnider, in a report. “These constraints have arisen from the inability of utilities to expand transmission capacity because of permitting delays, supply chain bottlenecks, and infrastructure that is both costly and time-intensive to upgrade.”

Opposition to digital infrastructure projects has also grown over concerns around the facilities’ water and power consumption—more than $64 billion in data center projects have been cancelled or delayed as a result of opposition over the past two years, according to research from Data Center Watch.

Still, these projects have generally received support from policymakers due to the strategic importance of AI and digital infrastructure. In July, the President Trump signed an executive order to accelerate the permitting of data centers on federally owned land.

“Policymakers increasingly view digital infrastructure as essential to national competitiveness in the technology sector and broader economy,” Thompson says. “This recognition has led to efforts in many jurisdictions to streamline permitting processes, accelerate power connections, and encourage investment in new capacity.”

Fears of an Overbuild

Some investors are wary that too much money is going into capital expenditures related to data centers. With hundreds of billions pledged, and questions arising surrounding the profitability of many large artificial intelligence models, the AI boom is starting to appear like a bubble to some.

“AI capex has become systemically important, carrying economic growth this year and sending the stock market to new highs,” says Oli Shale, investment specialist at Ruffer. “The hyperscalers have the benefit of the doubt but at some point, they will need to prove that the returns on these large investments will be accretive to their existing earnings. Currently, the race is on but high valuations give little wiggle room.” Shale notes if AI enthusiasm turns out to be misplaced, tech stocks, capex and economic activity could all turn down together.

“Here in the U.S., we’re a little bit concerned with the amount of capital that’s gone into data centers and some of the speculative building that’s going on,” says John Nicolini, head of real assets at Verus Investments.

Nicolini notes that many hyperscalers have clauses in their data center contracts that allow them to walk away from a project if they no longer need it. “They have the option at the end of the contract to walk away, the data center owner doesn’t have that option, he’s stuck with a data center.”

Data centers are far from being oversupplied, Thomson says. “Most major markets remain supply-constrained, with demand consistently outstripping available capacity. Moreover, the data centers are often contracted for 15-20 years with creditworthy counterparties, derisking the capital investment and protecting against downside scenarios for developers.”

Institutional investors should be prudent in manager selection and avoid managers who are overhyping the industry, Nicolini says. “Asset owners should be wary of managers who are hyping, [this] sort of inevitable growth in data center usage and power generation.”

As it stands, investors and hyperscalers are full speed ahead with building and funding data center projects. “The scale of what we’re seeing in terms of buildout, even if it’s half of what’s projected, is still just a massive stimulus to the demand side of the equation,” Boyce says.

Tags: Alternatives, Artificial Intelligence, data centers, electricity, Infrastructure