The gap between bottom- and top-quartile alternative investment managers is wide, causing endowments and foundations with similar asset class allocations to different managers to achieve different returns, emphasizing the importance of prudent manager selection, according to “The Implementation Gap,” a white paper from OCIO Analytics.

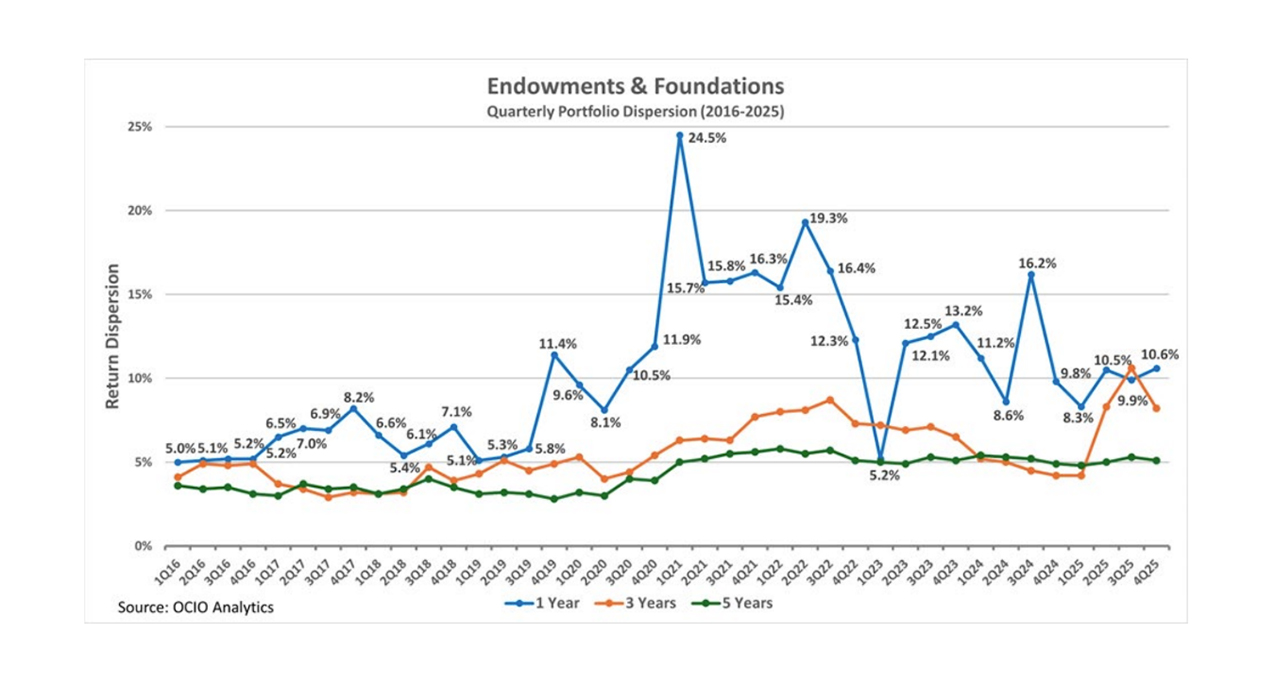

Return dispersion—the spread between the 5th and 95th percentiles of returns across institutions, which had stayed lower than 10% from 2016 through 2018—has been elevated since the pandemic, peaking at 24.5% in the first quarter of 2021 and remaining above pre-2020 levels through the fourth quarter of 2025.

A cause of this dispersion, according to the paper, is the widening gap between the effectiveness of top- and bottom-quartile alternative investment managers.

“A common narrative is that dispersion has increased because institutions have allocated more to private markets and other alternatives,” the white paper stated. “That explanation is incomplete. The role of alternatives has been well established for decades.”

“This [spread] is not a marginal consideration,” the paper continued. “It is the dominant driver of returns. Two portfolios with identical allocations can generate returns that differ by double digits—not because of what they own, but because of how well it was implemented.”

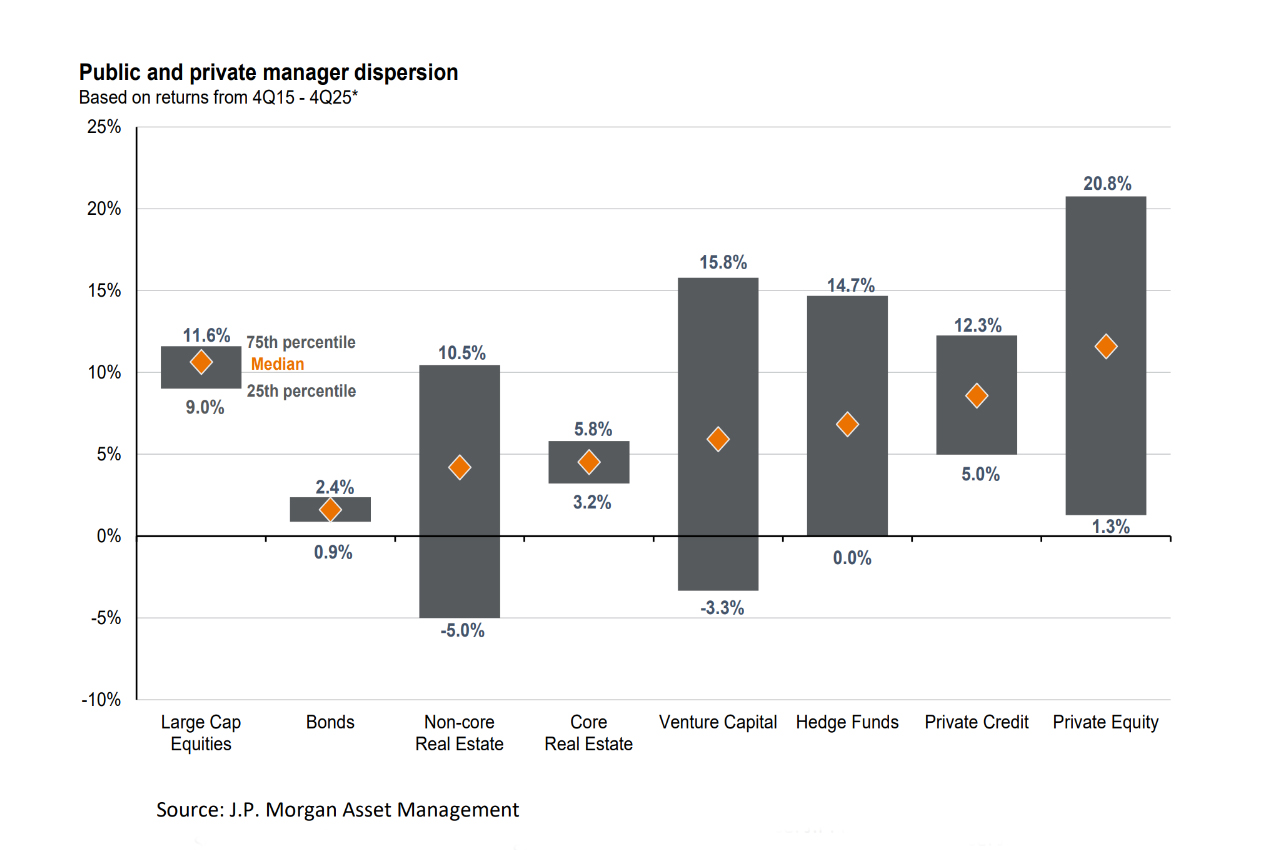

Among private equity managers, returns among 75th-percentile managers from the fourth quarter of 2015 to the fourth quarter of 2025 were 20.8%, while 25th-percentile managers returned 1.3%.

Other alternative asset classes saw similarly wide spreads between managers—with a 19.1-percentage-point gap between 25th- and 75th-quartile venture capital managers and a 14.7-percentage-point gap among hedge fund managers.

In comparison, top- and bottom-performing public-market managers had much smaller dispersion. Large-cap equity managers had a gap of only 2.6 percentage points between 25th and 75h percentile managers, while fixed-income managers had a gap of 1.5 points.

OCIO Analytics’ report noted that endowments and foundations—the types of allocators that typically have more than 30% of their portfolios invested in alternative assets—are therefore particularly susceptible to outlying performance or underperformance by their managers.

“Alternatives remain one of the primary drivers of top-quartile performance for endowments and foundations,” the white paper stated. “What has changed is not the relevance of alternatives, but the environment in which they are implemented. The opportunity set is broader, manager dispersion is wider, strategy complexity is greater, and capital flows into private markets have increased significantly.”

|

Market Commentary, Thought Leadership Influence Manager Selection |

|

How Manager Relationships and Transparency Standards Are Evolving |

|

What LPs Expect From Their Alts Managers |

Tags: Alternatives, investment performance, Manager selection