The illustrations of Bernie Madoff and Warren Buffett used on CIO’s February, 2015 cover and in the article entitled “The Riddle of Tampa Bay,” were not intended to suggest any similarities between Bowen Hanes or its principals and either man. We generally intended to depict the polar extremes of the asset management industry. CIO is not aware of any facts to support a comparison of Bowen Hanes or its principals to Madoff or to suggest that they have engaged in any fraudulent or illegal conduct, and the article did not contain any such facts. We have removed the illustrations from the article to avoid any misinterpretation. To the extent we may have unintentionally led our readers to believe that Bowen Hanes or its principals were similar to Madoff, or that they engaged in illegal or fraudulent conduct, we apologize.

We included in the original version of the article the following quote: “In my opinion,’ he wrote, ‘it is impossible for participants in the fund to assess the integrity of the plans’ investment or the plans’ ability to pay.’” Upon further review, we have removed it from the article.

The original version of the article misstated the frequency of the Tampa plans’ audits: they are annual, not every two years. We have corrected the article accordingly.

Finally, CIO is unaware of any past or pending SEC or other regulatory investigations or violations involving Bowen Hanes or its principals.

Crime seems a mild affair in Lady Lake, Florida.

Home to the world’s largest retirement community, the town sits a lazy 90 minutes northeast of Tampa Bay. Given the demographics, the local police force is compact. Recent criminal activity includes a counterfeit $50 bill proffered at the local dog groomers, several golf cart-related DUIs, and a scammer pretending to be retirees’ grandson asking for $2,000 to repair his car. Miami, it is not.

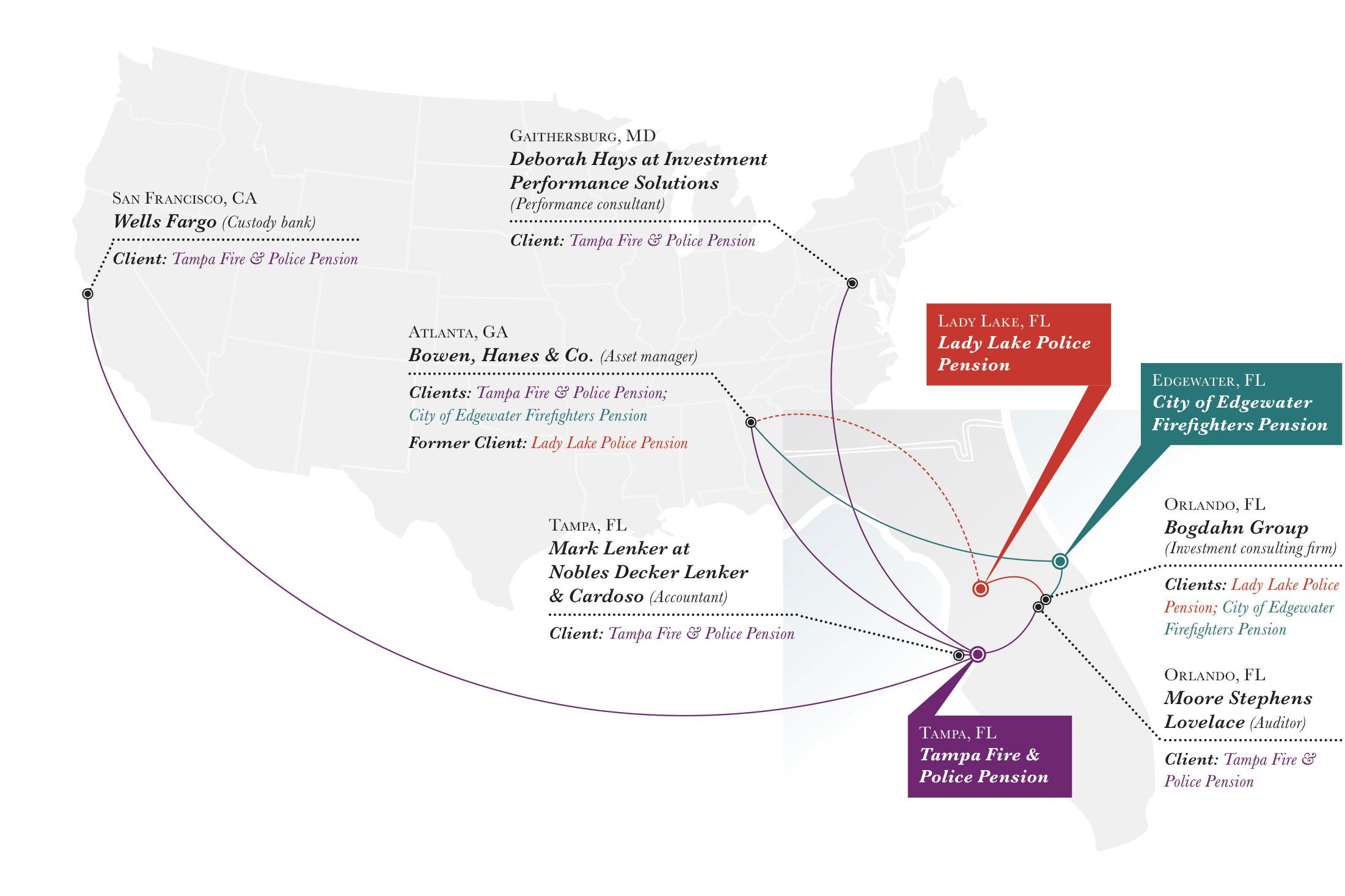

Like the larger force down the road in Tampa, the police tasked with protecting the citizens of Lady Lake from such scourges have a pooled investment account that will one day pay for their retirement. And like the police of Tampa, they have for years entrusted 100% of this money to a single manager: Bowen, Hanes & Co. of Atlanta, Georgia.

Or, at least, they used to.

On June 12, 2013, Lady Lake’s Police Pension Board gathered in the town hall for what was supposed to be a typical quarterly meeting. Four board members and three town staffers were present, along with the fund’s lawyer and its investment consultant, David West. Also present was their money manager, represented by Bowen, Hanes’ deputy David Kelly.

Public pension board meetings are predominantly dreary affairs. Consultants deliver the latest investment figures; managers review markets; invoices get approved; board members occasionally nod off. But by the time consultant West of the Bogdahn Group mentioned he had “an administrative item to bring up,” no one was sleeping.

West’s firm had been looking into Bowen, Hanes’ investment practices on behalf of a number of public pension clients. What it found was troubling.

Bowen, Hanes “do not appear to be keeping up with other managers’ industry standards, trading procedures, and compliance procedures,” West said. Bogdahn had been “comparing other managers’ operational procedures to Bowen, Hanes’,” and found the latter lacking. A state-of-the-art back office system “minimizes error, potential error, and provides for more sound accounting, fair allocation of trades, and minimizes dispersion.” Bowen, Hanes had no such system in place.

West told the board that he had no issue with the manager’s long-only investment strategy, and stated that “they are not doing anything illegal.” Even the recent lagging performance would not justify what amounted to an exceedingly rare move by a consultant to recommend firing a fund’s primary manager. Bogdahn’s issues with Bowen, Hanes were administrative, West said, not personal. Although the firm’s dated website advertises that it sets “the industry standard from a trading and portfolio accounting standpoint,” Bogdahn felt otherwise. “Bowen, Hanes’ operational infrastructure is lacking in state-of-the-art systems for portfolio compliance procedures and trade settlement procedures,” West said. For this reason, he advised Lady Lake to find new money management.

Then, incredibly, things got even weirder.

Bowen, Hanes’ Kelly asked the pension’s lawyer how often Bogdahn or any investment consultant really needed to be involved with the fund. State law required once every three years, the attorney said, but it was his “opinion that having a third-party consultant reporting on the manager’s performance is a prudent thing to do.”

Kelly disagreed. “Every three years is enough,” he argued. Kelly had handed out a letter from his firm’s president detailing issues between Bowen, Hanes and Bogdahn, who share a number of clients. The money manager had made a decision not to actively engage and work with investment consultants, including Bogdahn—a move unheard of in this industry.

Then came the ultimatum: “If the board chooses to go the multi-manager route with Bogdahn Group quarterbacking the plan, then Bowen, Hanes will resign.”

Lady Lake’s lawyer, likely incredulous at this turn of events, tried to clarify what was happening. “Mr. Kelly,” he asked, “if the board keeps the Bogdahn Group as its consultant, will Bowen, Hanes then resign as the fund’s manager?”

Yes, Kelly confirmed.

Lady Lake fired Bowen, Hanes. A few months later, taking Bogdahn’s recommendation, the board invested its $5 million between two new managers.

Like a bad rash, Bogdahn’s consultants have stayed on Bowen, Hanes, advising public pension clients across the state of Florida to take their money elsewhere. Although the consulting firm’s president declined an interview, public records attest to an effective campaign. The City of Hollywood’s Firefighters’ fund pulled its entire $15 million investment in 2012. In 2013, Venice’s police pension board voted 5-0 to heed Bogdahn’s advice and look at new management options. And just a few months ago, a Bogdahn consultant urged the City of Edgewater’s $10 million firefighters’ fund to rethink the risk it shouldered by having all its eggs in Bowen, Hanes’ basket.

But at one of the largest retirement funds in the state—the $1.9 billion Tampa Fire & Police Pension—there’s no Bogdahn to press this message.

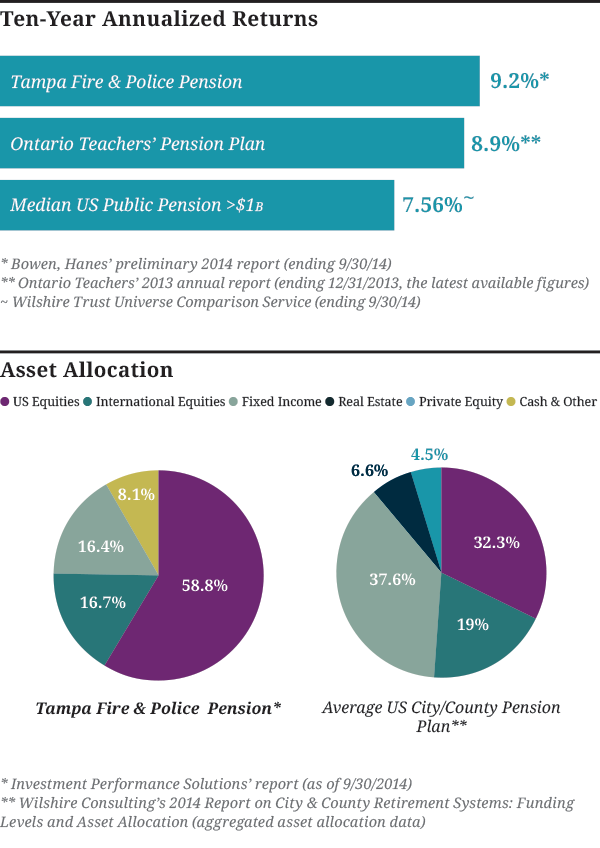

Since 1974, Tampa has done what most in the industry consider unthinkable. Casting aside the sacred tenet of diversification, the fund’s board entrusts all of its members’ retirements with a single money manager. And Harold ‘Jay’ Bowen III—and his father Harold Bowen II before him— have delivered, fabulously so. Tampa’s 12.3% annualized returns under Bowen, Hanes make it not only the most strangely managed public pension in America, but also perhaps the best performing. The massive and acclaimed Ontario Teachers’ Pension Plan—think Harvard to Bowen, Hanes’ community college—touts itself as the highest earner among major institutional investors worldwide. But the five-person shop in Atlanta beats Ontario Teachers’ in the short game (22.1% to 10.9% last reporting year) and the long (9.8% versus 8.9% over 10 years). As one elderly former firefighter told me, “Mr. Bowen and his father have worked miracles.”

A young ex-Marine, the elder Bowen arrived in Tampa in 1974, responding to an emergency. The city’s pension for police and firemen was in shambles: New widows found their monthly checks cut from $100 to $50, and the fund was on a steep path to flat broke.

“‘Your fund is so badly maintained and unsound that we’re putting you on notice: Unless you do something drastic, we’re going to withhold our contribution.’ That’s what the State of Florida told our trustees,” remembers Robert Smith, 76, the only person still alive and sentient who knows firsthand how the Bowen, Hanes-Tampa marriage began. Smith joined the force in 1960 and would later rise to chief of police and the city’s head of public safety. But as a newly minted corporal in the mid-1960s, he belonged to a younger generation of officers who were “a little bit frustrated” at the old guard’s handling of their retirement savings. He won a spot at the table, the youngest-ever trustee at that time, and set about putting the emergency workers’ financial house in order.

“All the money that was put into the fund went into treasury bills—not stocks,” Smith says. “Several of us trustees got to thinking that we had to do something, but knew we weren’t smart enough to do this on our own. So we had to hire expert advice—actuaries, lawyers, and investment counselors. And at $2 million or $2.5 million, quite frankly there were not that many people interested in dealing with a bunch of police and firefighter trustees.”

But for Harold Bowen II, the fund represented both a known quantity and an opportunity. He had worked with Tampa’s board at his previous job, and recently had founded his own investment shop, Bowen Management Co. The North Carolinian was also free of political ties. The board had looked at fellow police funds, and found most of these tight provider-politician networks were not worth emulating.

The Players: Who’s Who in the Tampa Pension Story

“He was obviously a man of high integrity, a very honest person,” Smith recalls. “I know this sounds silly, but when you’re in law enforcement, people are always trying to give you a smoked ham, or tickets to this or that. It always made me feel like those people were after something. And Harold only ever offered his investment advice.” The board hired Bowen as the fund’s sole manager—not at all unusual given the time and the meager size of the asset pool. “Then,” Smith says, “we started making money.”

For the first 12 years under Harold Bowen II’s control, Tampa’s stock portfolio beat the S&P 500 every single year. Twenty-nine years later, there is still nothing fancy about Bowen, Hanes’ approach. Current President Jay Bowen—Harold’s son—takes pride in that. Like his father before him, he’s an old-fashioned, value-oriented, buy-and-hold stock picker who identifies broad economic themes and trades on them. Bowen, Hanes doesn’t short sell stocks. It doesn’t mess with derivatives. It doesn’t focus on fixed income, except as a hedge for its equity holdings. While the vast majority of institutions have diversified into hedge funds, private equity, and real estate, Tampa remains all in on public markets.

And Bowen’s stock picks tend to be phenomenal. The firm’s 190,000 shares of Union Pacific Railroad, for example, have gained nearly 1,000% since purchasing them more than a decade ago. All told, Tampa’s stock portfolio has returned a cumulative 26,523% since 1974, while the S&P 500 gained just over 10,000%. That’s an average of nearly 250 basis points a year above its benchmark—for 41 years.

Despite this long and stellar track record, no large institution has ever hired Bowen, Hanes. Tampa is one of 115 clients, but still represents nearly three-quarters of the firm’s assets.

Mike Milken. Long-Term Capital Management. The dot-com bubble. Enron. 2008. Bernie Madoff. 2009. Kick-back and pay-to-play scandals at pensions in New York, California, Rhode Island, and Illinois. The list goes on.

In the 41 years since Tampa signed over its pension fund to Harold Bowen II, the investment industry has radically transformed. Risk has replaced returns as the guiding principle for managing institutional money. Investment firms shovel money into staff and infrastructure in pursuit of the all-important “institutional quality” designation. While Park Avenue Masters of the Universe were once the primary source of capital for hedge funds and other active management vehicles, it’s now pensions, university endowments, charitable foundations, and sovereign wealth funds that sign the checks that turn investment millionaires into billionaires. These institutions—public pensions most of all—want to see a multi-year track record of outperformance before even letting firms in the door. Industry types often describe the manager due diligence process as “opening the kimono” to potential clients. But to secure one cent from many public funds—those made ultra-cautious by two decades of scandals and crashes—hopeful managers not only open their kimonos, but drop them on the floor.

For Chris McDonough, head of New Jersey’s $79 billion retirement system, reaching that level of security with a sole manager would be a tough sell—even, he says, when he served as CIO of Philadelphia’s (relatively) smaller $4.3 billion pension. “It is difficult to envision a situation in which I would have been comfortable allocating all of our assets to one manager,” he says. “The investment risk would be too great to have one manager overseeing the entire fund.”

Nearly every public pension with upwards of $1 billion has at least one full-time, internal investment expert responsible for ongoing scrutiny of its managers as well as a professional consulting firm on retainer to help out. The board of trustees—often the teachers, firefighters, and other civil servants whose retirements are at stake—further acts as a check-and-balance on the staff and consultants. “Having a trained investment expert reduces risk of poor investment decision making,” says former US Securities and Exchange Commission (SEC) attorney Edward Siedle. He published a column in 2013 on Tampa’s unorthodox pension operation, remarking that “red flags abound” at the fund.

In Tampa, there is no investment consultant and no in-house asset management professional. Florida law requires police and fire pensions to “retain a professionally qualified consultant who shall evaluate the performance of any existing professional money manager and shall make recommendations to the board of trustees regarding the selection of money managers.” Tampa pays Deborah Hays, an ex-Thomson performance analyst based outside Baltimore, Maryland, to prepare quarterly reports on Bowen, Hanes—although, in the past, board members have debated whether this complies with the manager recommendation law. Most public funds use a big four accounting firm or government treasury staff to prepare financial statements. Here, the fund’s books have since 1987 been done by Mark Lenker, a certified public accountant, and his small local firm. Tampa is its sole institutional client, according to Lenker.

The fund has had three auditors since 2006: KPMG, Ernst & Young, and now local firm Moore Stephens Lovelace. According to the plan administrator, Tampa changed providers both times to align with City contracts. An auditor’s role is to review financial statements and express opinions based on their audit, says New Jersey’s McDonough. Their aim—and by extension, a pension fund’s—is to “obtain reasonable assurances about whether the statements are free from material misstatements.” In his view, “it is healthy to have some level of turnover in the firm that audits your financial statements; however, constant turnover might be cause for concern.” (The sentiment that three auditors in eight years was a major red flag was expressed repeatedly during interviews for this story.)

Bowen, Hanes’ only direct oversight comes from the three firefighters, three police officers, and three city employees who volunteer to serve on the board. Even the City of Tampa, whose credit rating and local economy is closely tied to the health of its public pensions, has no say in the operation of the police and fire fund. I requested an interview with the mayor to find out his comfort level with the situation, and was told that the “board of trustees is solely responsible for the general administration and operation of the Fire & Police Pension Fund. The city administration and the city council are prohibited from interfering with the operation, financial policies, and investment decisions made by the board.” Independence from politicians is a hallmark of quality public pension governance. However, funds that keep politics at arm’s length don’t typically also isolate themselves from nearly all forms of investment expertise.

“We’ve never had the need for a consultant, so why spend the money when we’re probably not going to listen to them anyway?” Mark Bogush, a fire department district chief, has chaired Tampa’s pension board since last February. Fit and silver-haired, Bogush runs a trustee meeting and our interview with the efficiency of someone versed in more stressful tasks (like marshaling a fire brigade). “We go to the investment conferences and people come up to us and ask why we have only one manager, and why we don’t have a consultant,” he says. “Frankly, I would hate to make a decision based on one person coming in and saying, ‘You’re taking too much risk.’” Bogush repeats a phrase I hear from nearly every retiree, board member, or other stakeholder involved with Tampa’s pension: “If it ain’t broke, don’t fix it.”

Industry professionals have their own refrain in response to the tale of Tampa Bay: “If it sounds too good to be true, it probably is.”

The arrangement has aroused deep skepticism in the Florida investment community for decades, according to several local sources. In the mid-1990s, a local paper published a major series detailing questionable conduct by the pension system. The fund’s only foray into private assets was a package of North Carolina farmland recommended by Harold Bowen II. The brokerage and management contract went to a longtime friend of his, and the investment turned out to be “a pain in the neck” for trustees, according to several sources. Likewise, the article noted, the board selected the brother of its attorney to design its new headquarters.

But for most, the pension’s story came to their attention in 2013 and 2014, when the Wall Street Journal and New York Times both published articles on the “Oracle of Tampa.” Jay Bowen and the Florida fund he manages became industry-wide gossip.

“This is the Twilight Zone,” one regulatory expert tells me. “This manager is so good that Tampa can use only them; so good yet no one else wants to hire them?” And there’s the rub with Bowen, Hanes. Putting aside all of the internal oddities at Tampa—a fund that’s proven it is willing to go against the norm—why doesn’t this well-publicized sage, with returns to rival Warren Buffett, have investors pleading to give him money? Institutions are notorious performance-chasers. Yet despite a 41-year track record and returns for its largest client over the last 5, 10, and 20 years that put it in the top 1% of its peers, Tampa still represents nearly three-quarters of Bowen, Hanes’ $2.6 billion under management. Why anyone with such phenomenal numbers would fail to report to the databases commonly used by institutions to find managers—and why they would aggressively fight consultants, this industry’s gatekeepers, at every turn—befuddles many.

All told, Tampa’s stock portfolio has returned a cumulative 26,523% since 1974, while the S&P 500 gained just over 10,000%. That’s an average of nearly 250 basis points a year above its benchmark—for 41 years.

A respected CIO of a major US pension told me that if he were appointed head of Tampa, his first move would be checking that the $1.9 billion does, in fact, exist. And according to the latest records from the fund’s custody bank—the institution tasked with keeping major portfolios safe and accounted for—it does. Wells Fargo holds essentially all of Tampa’s assets in a custodial account, which had a balance of $1,902,693,234.14 as of December 31, 2014. Like the fund’s choice of manager, accountant, consultant, and auditor, Wells Fargo primarily works with smaller clients than Tampa. Institutions of its size and larger—most of which have admittedly much more complex portfolios than Tampa’s—broadly consider only four banks “institutional quality”: State Street, BNY Mellon, Northern Trust, and JP Morgan.

But the presence of assets held in custody doesn’t guarantee a fund or investment manager’s behavior is all aboveboard. “If you’re working with a professional bank—and Wells Fargo is very much in that category—the custodian can only report about what they know about,” says Griff Ehrenstrom, Northern Trust’s director of corporate and institutional services consulting. “The client will take their custody report and augment it with host of other data, including expenses and liabilities. On the performance front is where you can see flagrant departures from industry standards of calculating a rate of return.”

Bowen, Hanes’ returns for Tampa are exceptional, but they are not impossible, according to risk analytics firm Xenomorph. “While there are clear strengths to the Tampa pension fund returns compared to the S&P 500, these do not seem completely improbable, particularly in more recent years,” a report prepared for Chief Investment Officer states. “The returns from the pension fund’s S&P 500 stocks and those of the S&P 500 show consistently strong levels of correlation,” which has increased since Jay Bowen took over from his father in the late 1990s. Muted volatility—historically a hallmark of suspicious investment practices—is also absent from Bowen, Hanes’ return stream

But another question remains: Why is one of the best stock pickers alive content to earn fees of 0.25% of invested capital, while legions of hedge fund managers with inferior performance rake in 2% plus 20% of any gains?

“Jay doesn’t like hedge funds, and he doesn’t like securities investigations,” Bogush, Tampa’s board chairman, says when I put the question to him. “As for his loyalty to us, Jay could come in tomorrow and ask for more, but he doesn’t. Only Jay could answer why.”

So I asked him. Tall and thin, Bowen has alert blue eyes and remarkably blond hair for his 53 years. Both times we meet—at Bowen, Hanes’ Atlanta offices and a Tampa board meeting—the long-distance runner is sharply dressed in a dark suit, French cuffs, and a gold watch, with a starched white handkerchief in his breast pocket. In suburban Atlanta, a stack of monogramed Bowen, Hanes coasters sit on a small office conference table. A built-in bookcase brims with volumes such as Ann Coulter’s Godless: The Church of Liberalism. I also spot something I haven’t seen in decades: two late-model typewriters, one at the receptionist’s desk and the other in an office.

While Jay Bowen has run day-to-day operations for nearly 20 years, Harold Bowen II, now 84, still maintains an office at the headquarters. His desk looks odd, and it takes me a minute to figure out why: There’s no computer.

The elder Bowen’s influence apparently reaches beyond the corner suite, suffusing the firm’s entire strategy. “My father decided a long time ago that if clients were going to entrust us with their entire fund, another feather in the cap should be a low, flat fee,” Bowen tells me. “And obviously, our fee goes up as the assets grow.” This model—one institution, one manager—depends on “total, complete discretion within the guidelines of a fund’s investment policy. When you have the multi-manager approach, inevitably you get put in a box.”

Yet even staying within the box of clients’ investment policy statements—documents stipulating asset classes and weightings a manager can take on—has proven challenging. In yet another episode of manager versus consultant, Bowen, Hanes’ David Kelly pushed back at the consultant’s attempts to bring the City of Edgewater’s$10 million pension into compliance ahead of an audit. This would have required meeting a minimum bond exposure. “I would consider the cash part of fixed income,” Kelly told the audibly confused trustees, before complaining bitterly about the prospect of selling stocks to meet the strictures. “This isn’t really about compliance,” Bogdahn’s consultant countered, while noting that the letter of the law was in fact very clear. “It’s about prudent management and risk. You are heavily overweight in stocks, and the market has run up tremendously. Are we at the top? I don’t know. But we might be. The time to rebalance is not when we’re at the bottom and it rebalances itself.” After nearly an hour of debate, the board passed a motion requesting that Bowen, Hanes “be in compliance at all times” with the fund’s rules.

Compliance may prove a larger headache for Bowen, Hanes than it already is. According to a source close to regulators, the SEC is aware of Tampa’s unusual arrangement with its manager, and the questions surrounding it. Jay Bowen says the SEC’s last visit was in March 2009.

When I asked, he declined to provide me with Bowen, Hanes’ composite returns covering all of its clients, but said they do exist. “These returns are audited… and we are GIPS [Global Investment Performance Standards] compliant,” Bowen wrote in an email. “However, for SEC purposes, we do not show our returns on our website or advertise them in a public forum.” The firm has not generated net-of-fee performance figures, he continued, which are “required in order to have our GIPS performance formatted in such a way to distribute it publicly.” However, the same regulatory expert questions Bowen’s logic. “If all of a manager’s performance numbers are GIPS compliant, one would think that they would show them to the public,” he says. “If simply deducting 25 basis points from the performance is all that’s required, why wouldn’t you do that?”

Even if the firm has flawlessly upheld SEC standards, the former head of risk for several major financial institutions advises Bowen, Hanes’ clients to reevaluate their arrangement. “Hypothetically, if we began working for a fund in that situation, we would say, ‘Red flag, red flag, red flag. The ground is covered in red flags’,” he says. “A fiduciary can’t just say, ‘It’s working, so that must mean it’s okay.’ That is not a justification. You don’t just run a nuclear power plant with no off switch and say, ‘Well, it’s produced so much electricity for 40 years,’ and not acknowledge that there might be a core meltdown in the middle of Long Island.”

“This isn’t a game,” he continues. “They’re endangering the welfare of pensioners. Are you going to tell an 80-year-old firefighter to put his suit back on and go to work because the Sage of Atlanta blew himself up? Even if we give this guy the benefit of the doubt, he’s ripe for blowing himself up. And if you tell me there won’t be another financial crisis, you’re smoking crack.”

In the wake of the last crisis, Bowen, Hanes has performed magnificently for Tampa—but not for all of its investors. (Bowen, Hanes does not pool all investors’ capital; instead, each client has their own account.) A firefighter’s pension in Hollywood, Florida, gave the firm upwards of $15 million to invest in the stock market in 2008. Anything Bowen, Hanes could buy for Tampa it should have been able to buy for Hollywood: the investment was for “all-cap” equities. However, Bowen lost 15.9% of Hollywood’s investment during the height of the crisis—the 2009 fiscal year—while Tampa’s stocks fell only 10.2% over the same period. And since then, Tampa has more than recovered.

Not so for Hollywood. Four-and-a-half years after making their investment, that famed Bowen, Hanes performance hadn’t materialized. While Tampa’s returns place it in the top one percent of its peers, Hollywood’s portfolio was at the other end of spectrum. The Bogdahn Group, Hollywood’s adviser, pegged Bowen, Hanes performance in the 98th percentile. In other words, out of 100 similar pools of stocks, the portfolio would have done worse than all but two of them. The pension cut its losses and pulled what was left. Fortunately for Hollywood’s bravest, only 9% of their money was invested with Bowen, Hanes.

Yet Tampa Bay—one of investing’s brilliant strategists or luckiest amateurs—remains all in.