University and college endowments saw strong returns in fiscal 2025, the one-year period that typically ended June 30, following multiple years of muted or negative returns.

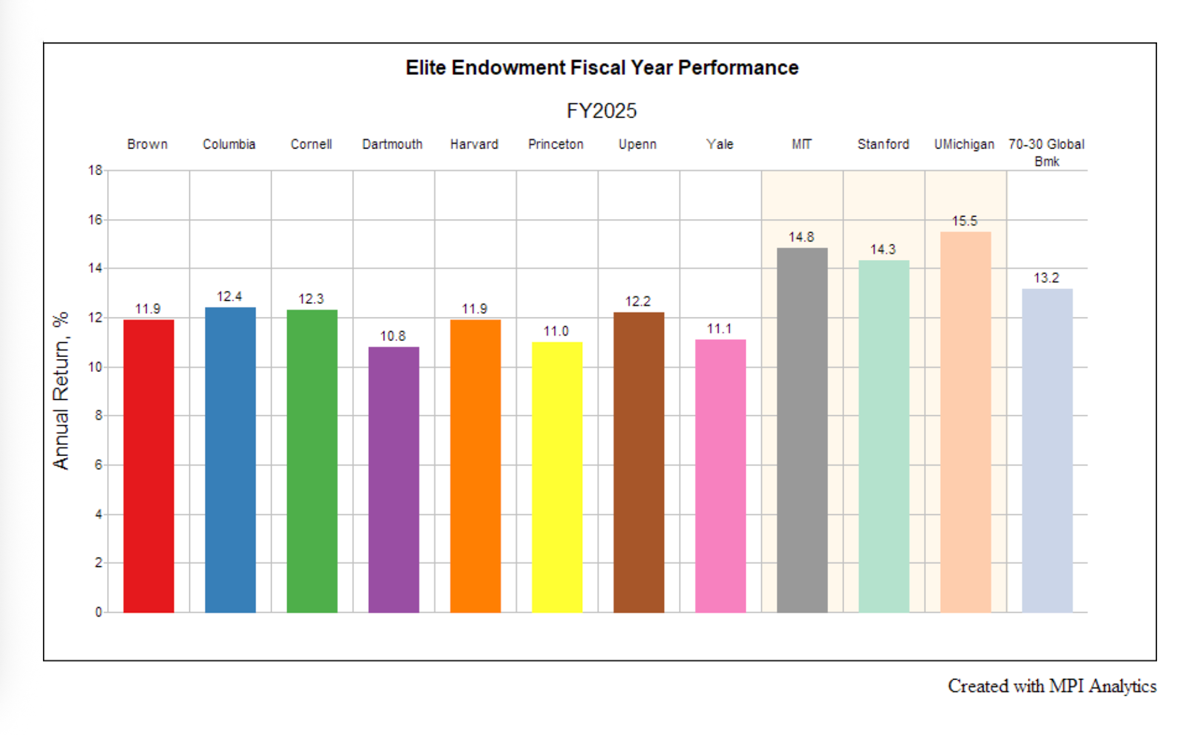

The average return of college and university endowments with at least $1 billion in assets last fiscal year was 11.5%, according to research from TIFF Investment Management. Across the board, nearly all asset classes contributed to total returns for the fiscal year.

Source: Markov Processes International

Key Drivers

“This year was unique, in that both risk and safety net assets had solid positive performance,” says Anne Duggan, a managing director at TIFF Investment Management.

Equities were among the biggest drivers of performance—the S&P 500 Index rose 15.2% during the year, but equity portfolios also benefited from global diversification, with the MSCI ACWI ex-U.S. index rising 17.7% during the year.

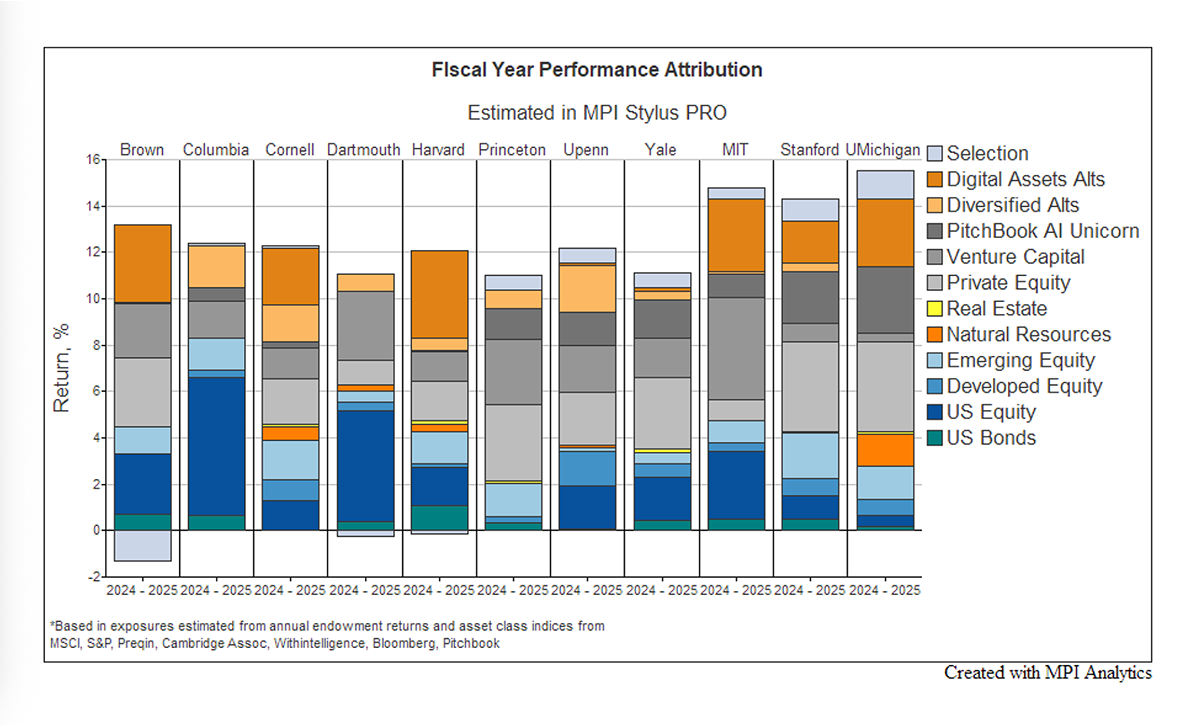

Several people familiar with the performance of many large endowments pointed to late-stage venture capital as a significant driver of the top-performing institutions’ private markets performance, benefiting from the booming valuations of artificial intelligence companies.

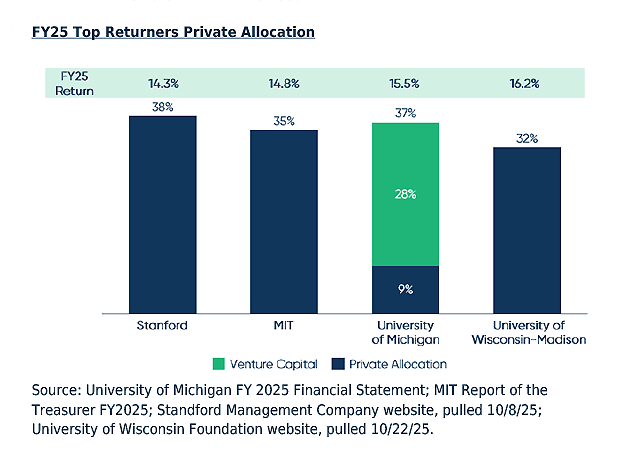

The University of Michigan, for example, with a 15.5% return, allocated 28% of its portfolio to venture capital, according to financial statements from the university.

Michael Markov, co-founder of data analysis firm Markov Processes International, which uses analytical tools to break down the return drivers of endowment portfolios, notes that strong performance came from endowments invested in themes like AI and digital assets.

Source: Markov Processes International

“Some of them, for a long time, have been investing in these themes,” Markov says, noting that the firm’s tools found that many large endowments saw strong returns from crypto investments and cryptocurrency hedge funds.

A report from MPI noted that several large endowments have investments in crypto funds and cryptocurrency directly—with the analytics provider estimating that digital assets returned 52.2% in the fiscal year and 83.2% in fiscal 2024. “That magnitude is enough to move total fund performance by several percentage points if you’re meaningfully exposed,” according to the report.

The report also noted that it is hard to tell how much of AI venture returns are cash-backed or marked-to-mark.

“We’ve already seen large venture franchises [mark up] AI-heavy funds aggressively without distributing anything … despite no meaningful exits,” the report stated. “That kind of internal markdown/markup flows straight into reported endowment performance, even though it’s effectively “paper.” So when we talk about AI exposure showing up in FY25, part of what we are likely seeing is unrealized, manager-set valuation. That matters for liquidity.”

Other Trends

Among the top-performing endowments that report their asset allocation, all had at least one-third of their investments allocated to private equity, according to TIFF. The University of Wisconsin-Madison, with a 16.2% return, had a 32% private equity allocation; Michigan allocated 37% of its portfolio to PE, including its VC holdings; and the Massachusetts Institute of Technology, with a 14.8% return, had a 35% allocation to PE.

Source: TIFF

Fiscal 2025 also marked strong performance in private equity and venture capital, after years when these asset classes were drags on investment performance. Private equity returned 9.7% during the year, according to TIFF, with VC returning 12.8%.

“It’s clear that the two-year trend of large private allocations being a detractor has come to a conclusion,” the TIFF report stated.

Yale University’s CIO, Matt Mendelsohn, noted in a statement that the university’s return (11.1%) trailed the returns of public indexes, as outperformance in several asset classes was tempered by lower returns in real estate and buyouts investments.

Fiscal 2025 performance of the Columbia University endowment “reflects the positive performance of global equity markets, and a portfolio of talented public markets managers who have skillfully invested in these strong markets and created alpha to enhance returns,” said Columbia Investment Management Co. President and CEO Kim Lew in a statement, noting that the fund’s private markets performance had a significant improvement, although it still lagged public market performance.

Colin Hatton, a principal in NEPC’s endowments and foundations practice, explained that the firm still expects private market assets to provide strong returns.

“Over the long term, we still believe that private markets will outperform the public markets,” Hatton says. “However, we’ve seen that turnaround the last three years. If you look at a 10-year time period, those with heavy alternative allocations did outperform, and if you go back beyond that as well.”

Liquidity and Navigating the Excise Tax

With a handful of endowments subject to an increased tax rate on their net investment income in fiscal 2026, as well as facing federal cuts to research and other funds from the administration of President Donald Trump, some institutions are re-examining their operations.

In the 2025 treasurer’s report, MIT noted it is considering “how best to respond to the substantial increase in the endowment tax and will continue advocating to maintain our decades-long partnership with the federal government to advance the nation’s interests through scientific discovery.”

In a statement, Yale President Maurie McInnis said the university would plan carefully, spend responsibly and implement contingency plans going forward, in response to the excise tax hike.

The excise tax will result in a small drag on investment returns, TIFF’s Duggan notes, but it will not be so big that major asset allocation changes will have to be made.

“The magnitude of the change is meaningful, but not so meaningful that you will see drastic shifts in asset allocation,” Duggan says. “You’re more likely to see tweaks around the edges in terms of asset allocation. I think when the tax was originally [proposed] at 21%, that’s when there was a lot of conversation [indicating the need for] radical change in asset allocation, but now that it is lower, only at 8% for the top ones, you’re looking at 30 to 50 basis points of tax drag.”

Using the Secondaries Market

Despite stronger returns in alternatives this year, some university endowments have tapped the secondaries markets to offload older vintage private equity investments, free up liquidity for capital calls, reinvest in newer themes and meet funding needs of their institutions.

In the face of federal funding cuts, multiple universities also tapped the municipal bond market to raise money for capital and other projects. Not all of the universities reported that the bond sales were prompted by any liquidity concerns in its portfolio.

Nicholas Tsafos, a partner in tax and advisory firm EisnerAmper, says the university endowments tapping the secondary market are likely liquidating funds that are closer to realization events, which could be a reason for some university endowments to receive favorable pricing on their secondaries sales.

Hatton notes that because secondary sales lead to a decline in the value of the portfolio—because the assets are generally being sold at a discount—endowments are examining how the haircut will affect spending and distributions to the university.

“I think another thing that institutions are thinking about is how it will affect their spending if they go and do a secondary sale,” Hatton says. “The effect that that can have on the spending policy and the support for the institution is another consideration that these groups are having to think through as they go through this.”

Related Stories:

Comparing Ivy League Endowment Returns

Endowments Could Turn to OCIO Amidst Tax Hikes, Liquidity Pressures

Endowments Face Liquidity Crunch Amid Market Pullback, Funding Cuts

Tags: Endowments