Asset Manager Consolidation Continues as Structural Shifts Reshape Industry

The asset management industry is experiencing an increase in consolidation as firms see a greater need to provide scale to their investors.

Global assets managed in the industry stood at $140 trillion as of the end of 2024, according to a November 2025 report from WTW’s Thinking Ahead Institute, the most recent data available from the firm.

Despite strong growth, the industry has faced several headwinds, including fee compression, the rise of passive management, and a decline in fundraising for many different alternative investment strategies—all of which have led to an increase in deals.

According to data from EY, financial services firms—including banks, insurers and asset managers—disclosed a total of 2,236 merger or acquisition deals in 2025, up minimally from 2,219 deals in 2024. Overall deal value, on the other hand, increased significantly, reaching $418.9 billion in 2025, compared with $282.1 billion in 2024.

Notable deals in 2026 so far include Nuveen’s $13.5 billion bid for Schroders, as well as the combined bid from Trian and General Catalyst for Janus Henderson. Asset managers are also scooping up asset class specialists as they seek to expand the types of products they can offer clients.

A report from Morgan Stanley and Oliver Wyman forecasted that through 2029, more than 1,500 M&A deals could occur among firms managing at least $1 billion in assets—reducing the number of asset managers globally by 20%.

The Need for M&A

When Nuveen announced its deal for Schroders, which would create a firm managing $2.5 trillion, Nuveen cited as motivation the scale it can achieve through a combination of both businesses.

“Larger firms are acquiring because scale matters more than ever,” says Dan Sondhelm, CEO of asset management marketing firm Sondhelm Partners.

The combination of Nuveen and Schroders, which manage $1.4 trillion and $1.1 trillion, respectively, would create the 10th-largest asset manager in the world, according to data from WTW. BlackRock CEO Larry Fink listed some advantages of his company’s acquisitions of Global Infrastructure Partners, which added $170 billion in assets under management, and HPS Investment Partners, which added $150 billion.

“In the last 18 months, we’ve welcomed an outstanding group of leaders from GIP, Preqin, and HPS,” Fink wrote in his annual letter to investors. “We have a long history of successful integrations, and a number of our current senior leaders joined us through acquisitions. We’re already benefiting from the fresh perspectives and experience of our new colleagues alongside our homegrown talent.”

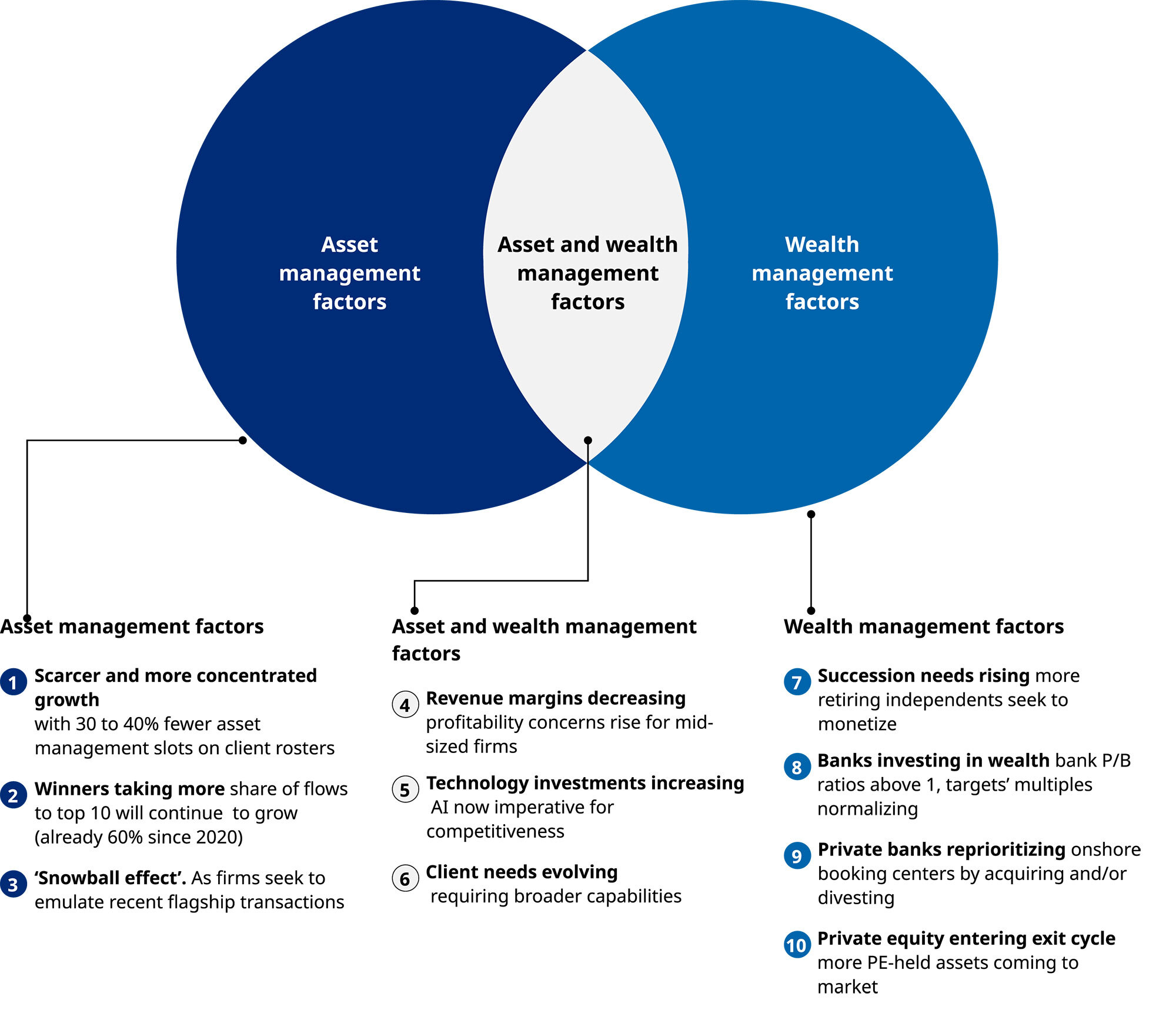

10 factors are contributing to the new wave of consolidation in asset and wealth management

Source: Oliver Wyman

Sondhelm says the increase in mergers has multiple benefits for firms who can capture more assets. “More AUM means more profit to reinvest into the business, and it helps firms hold their base when sales slow down or markets work against them,” Sondhelm says. Fundraising and asset flows have been consolidating at the largest asset managers, according to Franklin Templeton.

As private equity limited partners are increasingly writing larger investment checks to fewer managers, scale is also becoming a necessity to compete for mandates in private markets.“The thought is: If you’re not at scale, how do you compete more effectively?” says Christine Waldron, global head of fund and investor solutions at BNY.

A Morgan Stanley report identified three drivers of asset manager M&A: declining margins; rising demand and cost for technology and AI investment; and intensifying competition for capital. The firm also noted that clients are seeking more professional relationships with managers, while growth opportunities are becoming scarcer.

“We expect the combination of these factors to drive M&A in the industry,” said Betsy Graseck, Morgan Stanley’s global head of banks and diversified financial research, in a report. “Mid-sized players are becoming attractive acquisition targets for leaders seeking further scale and diversification.”

Who Wins in Consolidation?

At a time when asset managers are competing for less available capital, there are two clear categories of winners, industry experts note: asset managers with large platforms and scale; and boutique managers that can offer niche, but irreplaceable strategies.

“Institutional investors’ push to commit more capital with fewer funds and fewer managers is certainly a challenge for smaller firms, but it’s not necessarily an extinction story,” says Adam Bolter, a counsel at law firm Katten Muchin Rosenman LLP. “It accelerates a sorting of the industry into very large, multi-product platforms on one end and truly differentiated specialists on the other. Smaller managers that look a lot like the larger players, but without real scale or a distinctive edge, are the most vulnerable to consolidation. By contrast, boutiques that deliver hard-to-replicate alpha, niche expertise or clearly superior alignment will still likely have a seat at the table.”

Consolidation does not necessarily hurt smaller managers in isolation, notes Aaron Filbeck, a managing director at CAIA.

“In fact, it can benefit those with niche strategies or differentiated skill sets, since larger LPs may be actively seeking those qualities,” Filbeck says. “The challenge arises when a large LP’s capital overwhelms a smaller manager’s capacity, making the relationship impractical, regardless of how compelling the strategy may be.”

Most institutional investors utilize investment policies that limit them from investing with a manager, if the asset owner’s investment is more than a certain percentage of the manager’s total assets under management in the desired fund.

What LPs Think

Limited partner investors “are generally fine with consolidation, but they are not fine with surprise,” Sondhelm says. “They want the strategy to stay the same, the culture, the people they know, the level of attention they’re used to. Problems show up when messaging shifts, when the sales team gets distracted, when nobody knows who to call anymore. That’s when you start losing them. The managers who avoid that communicate early, stay consistent and make sure the investor experience doesn’t change before anyone has had a chance to [ask] why it did.”

Mark Pacitti, London-based founder and managing director of investment marketing and research firm Woozle Research, says, “The LP conversation behind closed doors is never what the public statement says it is. When a manager you allocate to does a big deal, the investment committee question is pretty simple: Does this change who is actually running my money? In more cases than you’d expect, the answer is ‘Yes.’ The follow-up question is: Why am I paying the same fees for a different team? Nobody has a great answer to that one.”

Pacitti notes that the firms that come out on top are those that are able to make acquisitions with real strategic fit and retain talent.

Some investors have expressed caution when a manager embarks on a new strategy or seeks an acquisition. In Janus Henderson’s most recent rejection to an acquisition bid by Victory Capital, Janus noted that its clients would have “significant reservations” if the firm were to merge with Victory. Bloomberg also reported that portfolio managers representing 90% of Janus Henderson’s AUM would consider leaving if a deal with Victory Capital were to go through.

Speaking during a webinar hosted by research firm Phronesis Partners, Bryan Hedrick, director of retirement investments at the Dallas-Fort Worth International Airport, said he was skeptical of public market asset managers that launched new private market strategies with no history of offering them.

Hedrick gave the example of one of his managers—which mainly offered public market strategies—offering a new private equity strategy out of nowhere.

“A few years ago, they decided to start a private equity strategy. Why? … The answer was, ‘We are identifying opportunities that wouldn’t fit in our mutual funds,’” Hedrick says. “Well, you’ve been doing that for 50 years. Why start now? Why get into an incredibly competitive market when everybody knows you this one way, and now you’re trying to say, ‘No, we’re not just that anymore’?”

Issues With Consolidation

Oliver Wyman research notes found that the success of asset manager M&A has been mixed—less than 40% of such transactions improved cost-to-income ratios three years after deals were finalized. The firm also found that half of those firms that acquired or were bought experienced net outflows. Additionally, half of private market specialists acquired by traditional asset managers grew slower than the market.

At times, asset managers may encounter operational challenges with technology systems or a misaligned data model across two firms.

“When firms acquire, you have a multitude of service providers that might already be servicing, and some of them may overlap; some of them may not,” Waldron says. “Now you end up having more oversight functions over more providers: You don’t have a single data model that you can leverage.”

With asset managers increasingly acquiring private market specialty firms, integration is often messier than the firms’ public statements suggest, Sondhelm says.

“Adding strategies through acquisitions makes sense. Building private credit or infrastructure capabilities from scratch takes years. Buying a team that already has the track record and the investor relationships is faster,” Sondhelm says. “You’re combining overlapping teams and figuring out who stays, who goes, or some mix of both. You’re merging products, you’re dealing with two cultures that didn’t choose each other.”

Post-merger outflows are often the norm, Pacitti says.

“The investment talent that made the acquisition attractive in the first place is usually gone within 18 months; integration costs get buried,” Pacitti says. “None of this shows up cleanly in the next annual report because nobody wants to say the deal didn’t work while they’re still trying to make it work.”