Asset Allocation

Lifting the Veil: How ESG brings transparency to the fastest growing markets

New research by index providers and other financial institutions suggests that emerging-markets companies with good ESG performance strongly outperform comparable companies in developing markets.

Reported by Debbie Carlson

Art by Harry Campbell

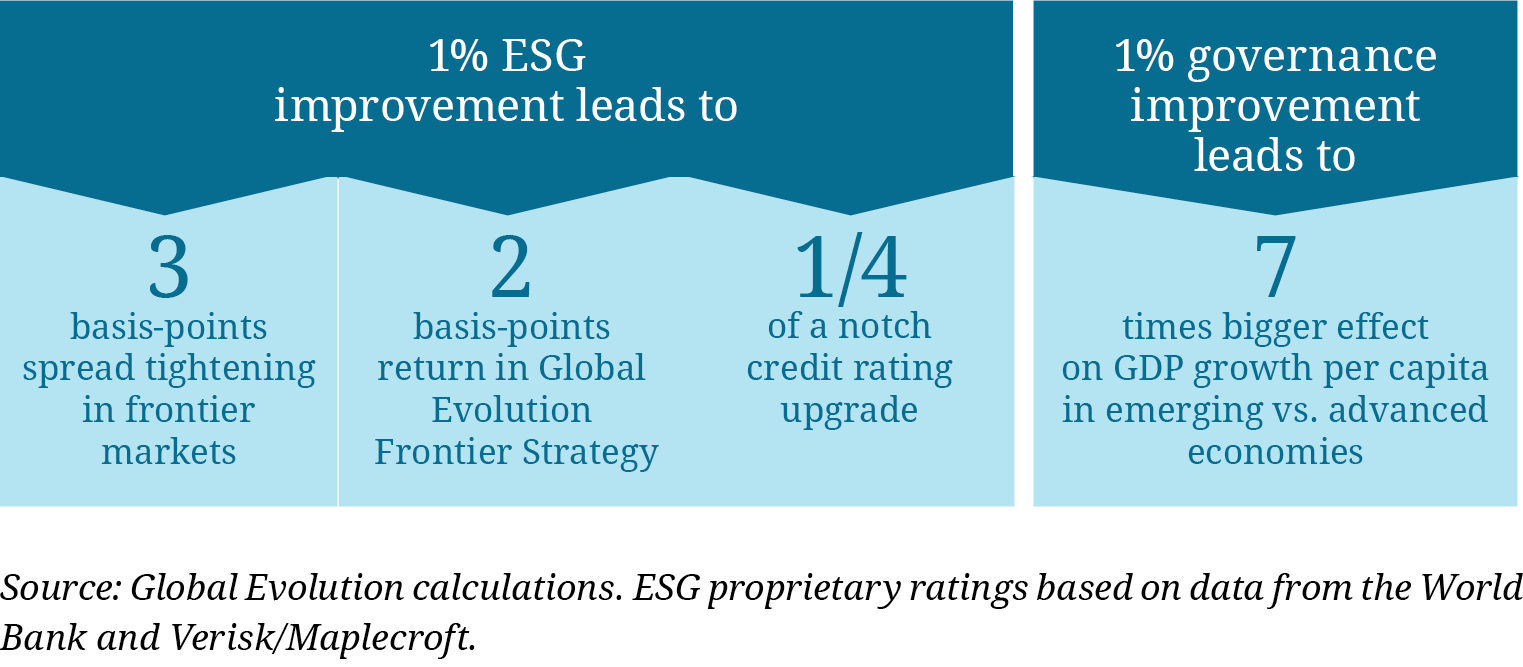

Until recently, there has been little evidence to support their use in emerging markets. New research by index providers and other financial institutions suggests that emerging-markets companies with good ESG performance strongly outperform comparable companies in developing markets. The transparency created when using ESG factors at both a country and a company level in emerging markets is key. ESG factors also account for a significant measure of the market variation between frontier- and emerging-markets bond spreads (see Fig. 1, page 36). However, “ESG use is still in its infancy, as I think only a few investors are looking at these factors,” said Nicolas Jaquier, emerging markets economist at Standard Life Investments, offering those who track it a chance to outperform.

When ESG analyses are publicized in emerging markets, they can help bring about investment-friendly cultural change, including reduced political corruption and higher standards of living that can produce both short- and long-term dividends in the form of reduced uncertainty for investors and a larger retail economy, several market watchers said.

“With most emerging markets, you’re dealing with a greater degree of information asymmetry where the companies or the government know more about what’s going on than they tell an investor, and any degree of data that enhances transparency tends to move a market quicker and more dramatically,” said Matt Moscardi, head of financial-sector research for MSCI ESG Research.

So overlaying ESG as alternate data has more impact. Cambridge Associates used data from the MSCI Emerging Markets ESG Index dating back to 2013 to examine the impact of ESG factors. The cap-weighted index tracks large-and mid-cap companies across 23 emerging-markets countries with high ESG performance scores relative to their sector peers. In its three-year existence, Cambridge found that it outperformed the MSCI World ESG Index by 367 basis points, annualized. While style and sector factors account for some of the difference, Cambridge attributed 199 basis points to stock-specific sources.

“ESG issues are core to a lot of what’s happening in EM countries,” said Eva Zlotnicka, sustainable investment research analyst at Morgan Stanley.

“The selection of stocks in emerging markets based on a broad measure of ESG quality has meaningfully contributed to the index’s outperformance over the three-year time period available for analysis,” Chris Varco, senior investment director, concluded in the Cambridge report. “Further, this stock-specific contribution has been consistent in a period when emerging markets were quite volatile.”

When Cambridge tested pre-index data using live MSCI ratings for select emerging-markets companies from 2007-11, the findings were similar: the Emerging Markets ESG Index outperformed the World ESG Index by 267 basis points.

“With the caveat that it’s a limited data set, it was exciting to show that as long as there’s been enough ESG data to use, it’s been crazy valuable,” Varco said.

What accounts for the greater impact of the “ESG effect”? “ESG issues are core to a lot of what’s happening in EM countries,” said Eva Zlotnicka, sustainable investment research analyst at Morgan Stanley. “Anecdotally, we think that the dispersion among EM companies is likely wider than what we see in many developed markets.”

When it comes to choosing countries to invest in, applying governance factors is a good starting point, Moscardi said, since strong governance factors aid transparency. “You can overlay it at a country level if for no other reason than to set your expectations of what you will find in that country,” he said.

Zlotnicka agrees, saying governance is the one component of ESG that is important in all cases.

Recent turmoil in some of the biggest emerging markets is creating more demand for ESG data as an indicator of stability or instability in the social and political realms.

“It’s not always more important than environmental or social factors, but is common throughout. I see it as a bit of a gating mechanism,” she said. For instance, a company with poor governance might not be able to handle environmental or social issues—or, conversely, to take advantage of positive environmental or social factors.

ESG Data Use Still in Its Infancy in Emerging Markets

Even in the publicly traded corporate space, only in the past several years has available research demonstrated the effect of ESG factors on emerging-market equities, said Lauren Compere, managing director/director of shareholder engagement at Boston Common Asset Management. ESG factors are likewise little used by most investors in emerging-market sovereign debt markets, Jaquier noted. For frontier markets, that’s even more of an issue, said Ole Hagen Jorgensen, director of research at Global Evolution, who also chairs an advisory committee on credit ratings for the United Nations Principles for Responsible Investment.

But recent turmoil in some of the biggest emerging markets is creating more demand for ESG data as an indicator of stability or instability in the social and political realms.

Jorgensen creates models to examine changes in hard currency spreads, using a combination of public and proprietary ESG data. The model includes 10 variables; nine are standard economic factors, and the tenth a composite of ESG indicators.

The model shows that 49% of market variation in frontier and emerging-market bond spreads is explained by economic and financial fundamentals. Adding ESG factors increases the explanatory power to 54%, Jorgensen said. “That’s a 10% improvement, more or less, of how our models can inform us of what looks to be undervalued or overvalued,” he said. “That’s a lot, and that 10% comes from ESG. So nobody can convince me not to include ESG dynamics. It gives us more information for the investment process. It’s as simple as that.”

“Revenues in Mongolia from copper production [flowing into] fiscal coffers [are] managed well. The incentives of the institutions are much better than they are in, say, Venezuela. There’s more transparency, less corruption, and more enforced property rights,” said Ole Hagen Jorgensen, at Global Evolution

Recent events are making these effects harder to ignore. “ESG in emerging markets is getting more attention [particularly with] governance,” said Jason Trujillo, senior analyst at Invesco Fixed Income. “Most notably, you can highlight the issue of Russia and Brazil.” Russia’s annexation of Crimea and its possible interference in elections in the US and elsewhere via hacking into computer systems, which reinforced longstanding distrust of the government, are examples, as is the Petrobras kick-back scandal that led to the impeachment and removal of Brazil’s then-President Dilma Rousseff.

ESG Dynamics Matter for Frontier Returns

Some asset owners and other investors are hesitant to incorporate ESG factors into their research because of a misconception that it’s hard to neatly quantify such issues as improving access to health care or gender equality, but Jorgensen disagreed. In emerging-market and frontier-market countries, progress to lower corruption, improve education, and properly use natural resources is an economic factor, he argues.

In these markets, the effort a country puts into improving its citizens’ living conditions creates a domino effect: generating greater economic activity, enhanced political stability and higher creditworthiness, he said: “Countries that come from low levels in terms of ESG also generate the highest returns in EM sovereign debt. There you have so many low-hanging fruits, even small policy changes, small improvements, can lead to big efficiency enhancements in the economy…Higher creditworthiness is linked to bond prices, spread compression, and higher returns. It’s not just about growth, it’s about sustainable growth.”

On the equity side, Liz Su, global equity analyst/emerging markets at Boston Common Asset Management, said ESG factors are even more important when investing in emerging markets because of the inherent volatility of the asset class.

“There is more potential to add alpha through ESG research and engagement,” she said. “It’s more an alpha factor in emerging markets than just a risk factor.”

Adding ESG to Econometrics

The graph illustrates valuation signals derived from Global Evolution’s econometric model for fair value of hard currency sovereign bonds in frontier and emerging markets. When signals breach one standard deviation from their vhistorical trend, there is a statistically significant buy or a sell signal which is based partly on ESG indicators and partly on macroeconomic, fiscal, and financial variables across all emerging market countries.

Turmoil Drags Down Turkey’s ESG Score

Asset owners who want to incorporate ESG data in their decision-making can begin by using publicly available information, such as country scores from the democracy watchdog Freedom House and governance scores from the International Monetary Fund and the World Bank, both of which include corruption indexes, along with smaller data sets that score countries on such factors as press freedom, the death penalty, and strength of institutions.

“The information is broadly publicly available; the issue is how do you interpret it and rank it against a peer group country,” said Trujillo. “A lot of the ranking systems, whether World Bank or Freedom House, are helpful in that they provide a bit of apples-to-apples ranking across a broad spectrum of countries.”

Governance is the primary ESG factor to consider in emerging markets, observers said, as better governance can help speed improvements in environmental and social factors. Better governance also tends to have the swiftest positive impact on investments, while social and environmental factors have greater impact in the long run.

“Of the three, I believe coming from a traditional EM investor, corporate governance is a critical factor in EM investments,” Su said. “Investors are willing to pay a premium for better emerging-market firms, and sometimes people are willing to invest in firms with better corporate practices that could make up for a country’s weakness.”

A CIO can tilt or combine factors as needed, depending on the mandates the asset owner applies, Jorgensen said. Different ESG factors have greater or less statistical significance in explaining change in spreads for individual countries.

Take Mongolia, where Global Evolution invests. This country has rich copper deposits, and as a frontier market is making strides in managing its resources better.

Georgia, an Eastern European country with healthy business indicators, is easing conditions for the private sector to do business.

“There’s an interaction between environmental and governance that can be a blessing,” Jorgensen said. “Governance plays a role in the management of the wealth and revenues. Revenues in Mongolia from copper production [flowing into] fiscal coffers [are] managed well. The incentives of the institutions are much better than they are in, say, Venezuela. There’s more transparency, less corruption, and more enforced property rights.”

Another example is Georgia, an Eastern European country with healthy business indicators that is easing conditions for the private sector to do business. “What’s really important for these countries to take off with growth and development is to have a flourishing private sector,” Jorgensen said.

Argentina is an example of an emerging-market country with good environmental and social factors, but where governance was lacking, Jaquier said: “Argentina had a very well-educated labor force, a lot that went abroad” during the presidencies of Nestor and Christina Fernandez Kirchner. With new President Mauricio Macri at the helm, Argentina’s governance is improving.

“They’re reviewing the whole procurement system, which was an area of large-scale fraud and corruption, so it’s encouraging that things are being done,” Jorgensen said. “We think that undoing some of these practices will help put the country on the right tracks.”

Pressure from leading companies is pushing some emerging-market governments in the right direction, Su and Compere say. “When we talk with corporate management about why they’re interested in ESG issues,” Su said, one reason is “they aspire to be global leaders. Their market cap is still catching up, but they aspire to adopt ESG best practices.”

Brazil provides another example. Stock exchanges in Latin America’s biggest nation are requiring more disclosure in order to get listed, which means more data availability and greater transparency, said Compere. In the finance sector, Uno Banco has this global focus. “They’re one of the few emerging-market companies that do integrated reporting, which means they do ESG as part of their disclosure,” she said.

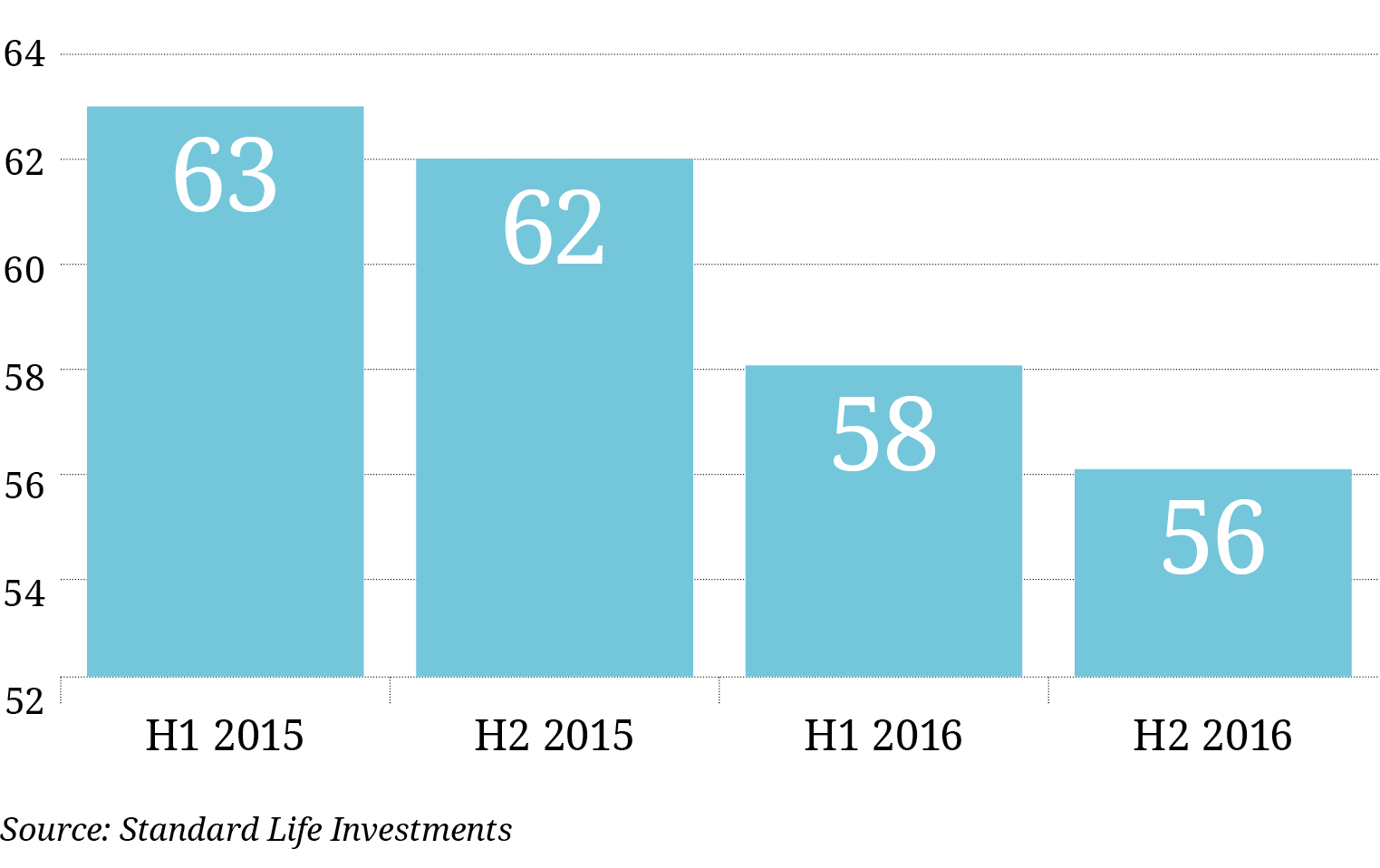

At the end of 2015, Turkey’s quantitative score was average; widespread political turmoil boiled up soon after, [but] these issues were not reflected in the price of Turkish assets at the time and credit-rating agencies had not downgraded their assessment of the country.

Brazil continues to feel the repercussions of the Petrobras scandal, which caused Standard Life to downgrade its ESG score. However, Jaquier said he’s now turning positive on the country, since the issue of corruption is finally being addressed, highlighting the strength of the judiciary system, and the measures being put in place to avoid another major scandal are encouraging. Moreover, investors that incorporated ESG factors into their decision-making on Brazil would likely have been unaffected by the scandal because lack of transparency prompts ESG investors to avoid state-owned enterprises like Petrobras.

Monitoring ESG factors and watching political changes can also give investors an early warning when the situation in a particular country is deteriorating, ahead of credit-agency downgrades, Jaquier said. In Turkey, for example, managers at Standard Life suspected the quantitative factors were out-of-date versus their qualitative judgment as to where the country was heading.

At the end of 2015, Turkey’s quantitative score was average; widespread political turmoil boiled up soon after, including protests, press crackdowns, allegations of corruption, concentration of power around President Recep Tayyip Erdogan, and an attempted coup. These issues were not reflected in the price of Turkish assets at the time, however, and credit-rating agencies had not downgraded their assessment of the country.

A closer look at Standard Life’s ESG score for Turkey, which began to slip in the first half of 2016 (see Fig. 3, above), would have at least partially cleared up this blind spot. “Turkey is a good example of how paying close attention to some of these issues can limit risk in your portfolio but also add value,” Jaquier said. Turkey’s situation and the rating agencies’ slowness to downgrade the country also reflect the degree to which country analysis is still focused on macroeconomic data at the expense of other relevant factors.

“I’m not saying [the macroeconomic view is] not important, because we also look at it,” Jaquier said. “For us, there’s a clear and obvious value-add to taking these softer indicators into consideration—especially in the political and governance areas, which are key behind a country’s willingness to address them.” CIO