Matthew McInerny

Timothy Rabe

CIO: We saw record issuance of floating-rate bank loans in the first quarter of 2021, and there’s still a heavy calendar of offerings ahead. What’s driving the appetite for this kind of debt?

Matthew McInerny: We believe we’re at an attractive entry point for this asset class both because it offers yield in a low-yield environment and because there is not a lot of distress in the market right now. In addition, bank loan performance historically correlates closely with inflation, which has been trending higher, and higher inflation tends to lead to rising interest rates that boost yields on floating-rate loans. At the same time, the Federal Reserve has indicated it may begin tapering its easy-money policies before year-end. If that happens it would likely drive short-term rates higher, too. We would then expect the average spread versus LIBOR [the benchmark interest rate at which major global banks lend to one another] in the loan market to widen a bit from the 417 basis points [bps] that prevailed in early September.

Timothy Rabe: We are in kind of a Goldilocks era right now. You’re seeing upgrades outpace downgrades and just about everything in the loan market is performing quite well. Even if fixed-income markets weaken, loans are at the top of the capital structure and backed by collateral, so recoveries tend to be higher than they are for unsecured bonds. However, we believe recoveries will continue to decline as there are now a growing number of borrowers who issue only in the loan market rather than in both the loan and high-yield markets.

CIO: How attractive is the new supply on the way, and what’s driving all the issuance?

McInerny: There’s about $60 billion of supply we can see. A lot of it will finance corporate M&A [merger and acquisition] activity, which is our preferred type of financing because there’s no sponsor involved, there are better credit agreement documents, and there are typically higher quality companies involved, often with BB credit ratings.

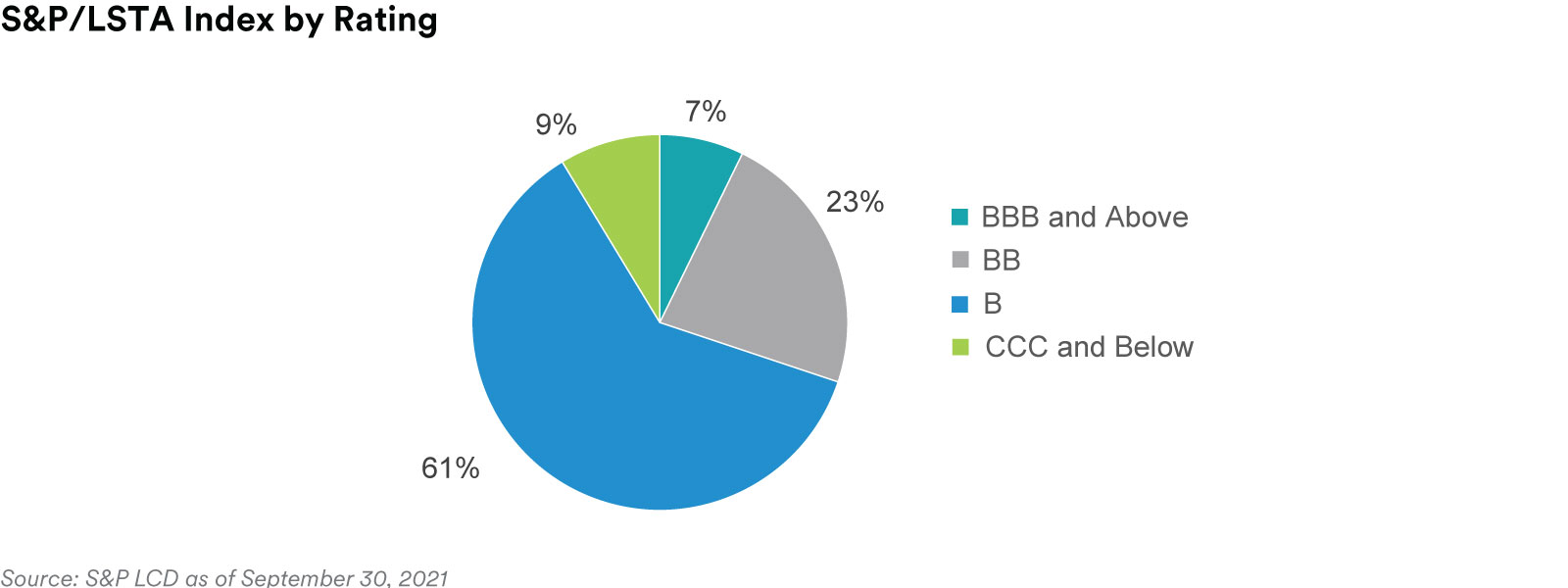

CIO: What does the market look like outside the BB sector?

McInerny: The market has four main categories. The investment-grade [IG] BBB sector represented about 7% of the market as of September 30. We believe that IG loan yields are attractive versus similar maturity US IG bonds. One notch down on the credit scale is the BB sector, which is about 23% of the loan market. Next are B-rated loans, representing about 61% of the market, up from 43% five years ago. These loans are popular financing vehicles for leveraged buyouts. The reason market share for this sector has risen so much is because collateralized loan obligations, or CLOs, have become a much bigger part of the market and CLO structures require, among other things, loans with an average rating of B. The final category is CCC loans and unrated loans, which includes defaulted loans, representing about 9% of the market.

CIO: Where are the best values to be found today?

McInerny: We are finding pockets of opportunity in BB loans, as well as within the single-B space.

CIO: How is the growth of CLOs impacting the opportunity for other investors?

Rabe: The key for a CLO is getting a diversified group of loans that fits its structure. Beyond ratings, it looks at factors such as recovery scores, industry, and market price—things that don’t always have to do with the underlying credit. That creates opportunities for us to look at loans that don’t work for a CLO, such as loans trading below 80% of par in times of market stress. Those loans may represent a great risk-reward opportunity for us.

CIO: Speaking of risk, what would you caution an investor to be mindful of when entering this market?

Rabe: The biggest misconception about bank loans is a belief in their inherent safety just because they are secured. Conventional wisdom says loans give you most of the upside of the high-yield market with much less downside. But over the past decade, a growing percentage of the market has come to be represented by borrowers who are issuing debt only in the loan market. In that case, they’re not much different than a high-yield issuer. Yes, their loans are secured by assets, but there’s often no subordinated debt in the borrower’s capital structure—no cushion to eat through before getting to the loans. On top of that, loans are callable at any time at 100 cents on the dollar, so your upside is basically zero if you buy near par. People sometimes get lulled to sleep with loans, but when all risk markets do poorly, loans participate almost as much as high-yield does. Also, the protections on loans generally aren’t as good as they used to be because so many loans issued today are “covenant lite,” meaning they have fewer restrictions on the borrower and fewer protections for the lender.

CIO: Should covenant-lite loans be avoided then?

McInerny: Investors should understand their characteristics, but we feel it’s neither smart nor practical to avoid them. Even when they don’t have maintenance covenants, loan credit agreements are generally still of higher quality than bond indentures.

CIO: How is MIM positioning its loan portfolios in this environment?

McInerny: In general, we believe you stay out of trouble in the loan market by picking the right credits. In a market like this, it’s extra important not to stretch to buy something in which you’re not properly being paid for the extra risk. Right now, we’re skewing toward high credit-quality loans because you want the ability, when the market does correct, to go lower in credit quality and buy securities that have become stressed or distressed.

CIO: How hard or easy is it to find the right credits?

Rabe: Unlike with public securities, borrowers don’t typically publish a lot about their financials once their loans are in the market. We believe that provides an advantage in the secondary market to someone like us, who vetted those loans before they were made and maybe even participated in them. It gives us information that may be useful later should the borrower, or even an entire sector or the whole market, have issues.

CIO: What distinguishes your approach to research?

McInerny: We have very experienced portfolio managers backed by a deep research team of 35 people. Our team leaders on average have more than 20 years of experience, including significant sector experience, which we feel is key as they’ve invested in those sectors over different economic cycles. We believe that can help gives us an advantage when the market sells off; there are certain credits we suspect are going to get oversold, that we’re going to want to add to our portfolio. Another feature at MIM is that we have a research team in London, which helps with investing in European cross-border issuance.

CIO: How else can strong research add value?

McInerny: Our depth and experience allows us to be active in the middle market, which helps us add value for our clients. For example, we had a middle-market issuer come to market recently with a loan; we were heavily involved in negotiating the credit agreement and inserting meaningful improvements to protect investors. Those types of opportunities can potentially add alpha to a portfolio, but you need an experienced and deep research team to dig through those credits and find the ones that make sense. Some CLOs prohibit middle market loans in their portfolios.

CIO: Do you see any advantages for investors to participating in the bank loan market outside of structured products like CLOs?

Rabe: Although the market has been on an even keel, we expect even more attractive opportunities the next time it goes down. When it does, we’re going to have the capacity and resources to put capital to work. When you own a highly diversified loan portfolio with a lot of different issuers, the way a lot of CLOs do, you’re going to have a lot of distressed issues to work through in a downturn, which can stop you from allocating capital on the other side. We seek to avoid that by holding a portfolio that is relatively concentrated with the goals of avoiding credit risk and having the time and capacity to put capital to work at lower levels.

CIO: How is this reflected in portfolio performance over the long haul?

Rabe: While a larger loan portfolio may tend to track the loan index fairly closely, our more concentrated portfolio seeks to drive performance with strong security selection. An investor might want to ask whether they are simply searching for blanket exposure to the loan market or alpha inside that exposure. We’re trying to deliver alpha inside the exposure.