Keeping your deficit under control

For materially underfunded plans, the key strategic imperative right now is to ensure that your deficit remains ‘solvable’ in order to manage the risk of unexpected contributions.

In other words: you don’t want your investment problem to become too large. With this in mind, we believe managing interest rate risk is still an important consideration to protect against downside funded status shocks.

Hedging to keep your problem ‘solvable’

As interest rates and (in some cases) funded statuses have trended lower, the natural reaction of plan sponsors could be to consider pausing their interest rate hedge paths and waiting for rates to return to more ‘normal’ levels.

It is true that pension deficits would fall if interest rates rise, but consider that hedging would potentially stabilize the required excess investment return (over liabilities) required to solve the deficit problem.

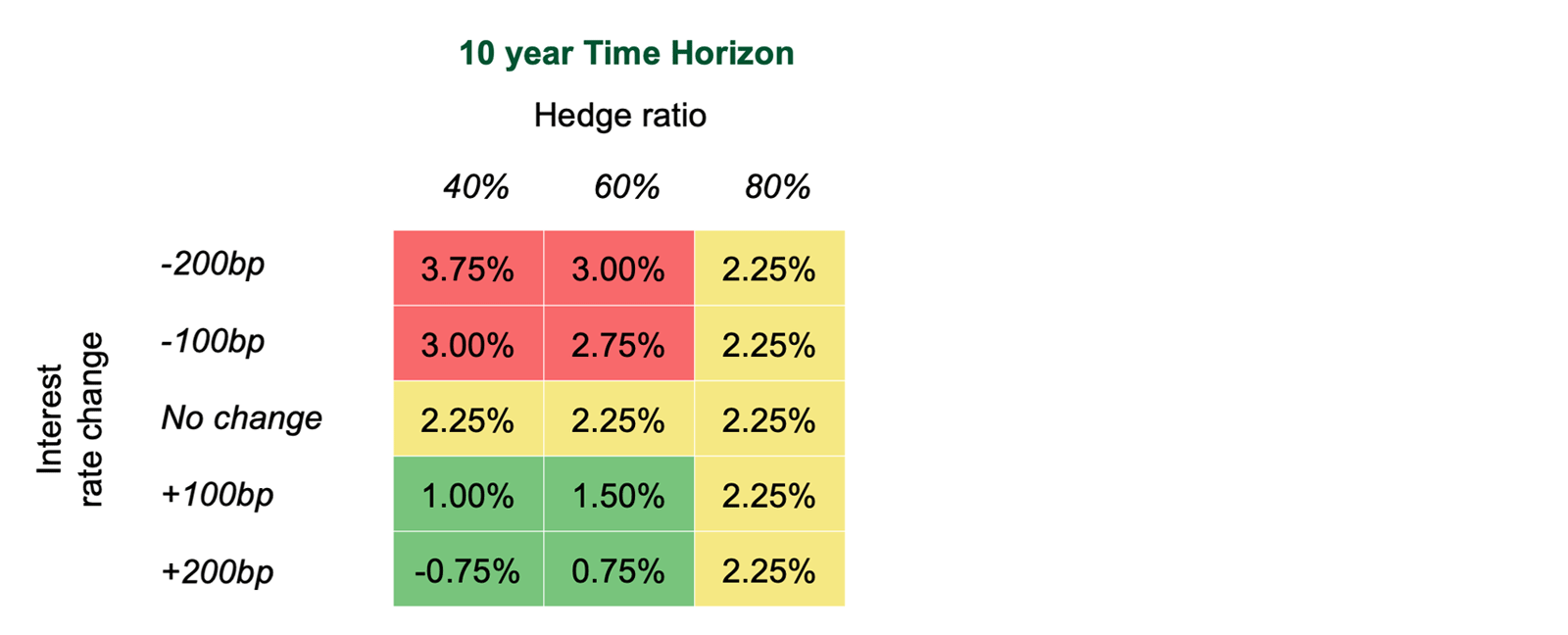

Let’s consider the hypothetical case of an 85% funded plan1 – completely closed to any future benefit accrual and paying out 6% of its assets annually to meet benefit payments.

Figure 1 shows the excess investment return required every year to close the funding gap over a 10-year horizon – while considering different interest rate scenarios.

Figure 1: Excess return (pa) to close an 85% funded status gap1

The yellow shaded boxes show that a higher hedge ratio, in all cases, helps stabilize the required excess return and helps avoid scenarios where the required return can become too large (potentially requiring contributions).

“OK, so I understand, but I’m still convinced that rates will go higher”

We certainly empathize with investors that believe that rates are more likely to rise than fall.

However, we also believe that it would be a mistake to place all bets on rates going higher. First, interest rate forecasts have a poor record. Second, although rates are low, they can go even lower.

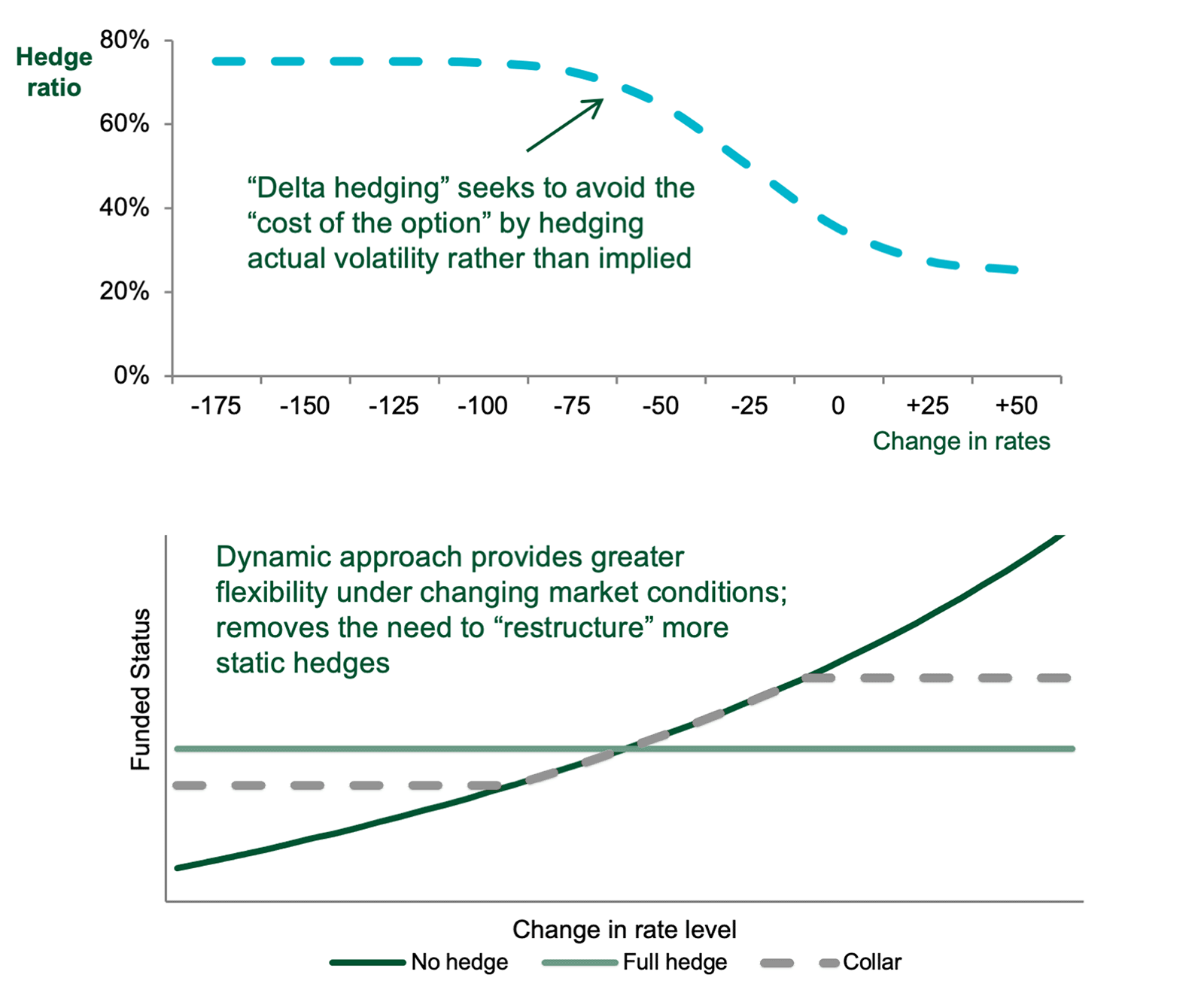

To mitigate the potentially sizable cost of being wrong (see our three reasons to be cautious below) it may be worth considering an asymmetric hedge. This is a strategy designed to benefit if rates do rise, but with a protective stop loss if they fall.

There are two ways to do this (1) through a downside interest rate swaption strategy or (2) through an interest rate swaption collar strategy (Figure 2).

Figure 2: Downside protection strategy and interest rate collar strategy2

Option strategies often understandably invoke cost concerns. However, option premia tends to be less significant for interest rates – as there are both natural buyers and sellers of protection. There are also are many ways to ‘cheapen’ the cost of the hedge such as dynamic delta hedging or option replication strategies.

Reasons to be cautious – three ways low rates amplify funded status risks

1) As rates go down – interest rate sensitivity goes up

A pension liability represents the amount of funds an investor would need to hold today to meet its future cash flows, typically on a bond matching basis. This means that the present value of liabilities is sensitive to interest rates, with lower interest rates meaning higher liabilities and vice versa.

In turn, as liabilities increase, so does the interest rate sensitivity. This can be demonstrated by taking the average plan, whose sensitivity to a basis point move in the interest rate yield curve has doubled over the last 10 years (Figure 3).

Figure 3: Interest rate risks have risen as rates have fallen: Dollar Value of a Basis Point (DV01)3

From a risk budgeting perspective, this means plans have had to increase their hedge ratios just to maintain the same dollar risk position – in effect moving just to stand still.

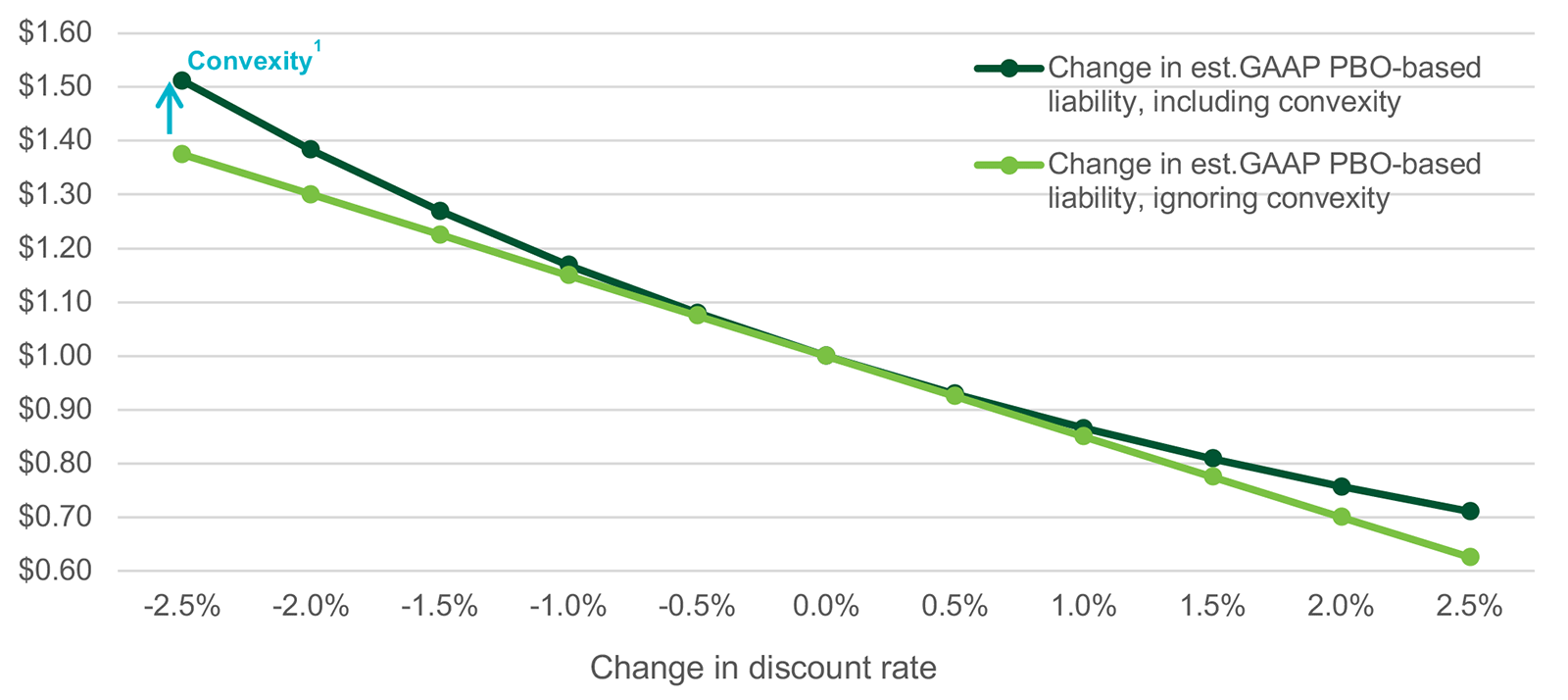

2) Convexity tilts funded status risks to the downside

The interest rate sensitivity of a pension liability is not fixed and is itself sensitive to the level of interest rates. This is a property known as ‘convexity’. What this means in practice is that there is more downside dollar exposure than potential upside for every basis point move in the interest rate curve – a phenomenon that makes interest rate sensitivity an asymmetric risk.

This asymmetry is higher for a fall in rates than it is for a rise in rates. So, small changes in interest rates become more meaningful for liability valuations when interest rates are low (Figure 4).

Figure 4: Convexity can amplify the downside impact of rates relative to the upside4

Think of interest rate sensitivity as the speed at which liabilities change, and convexity as a measure of acceleration of that change. For the unhedged plan, convexity accelerates downside funded status risks, but decelerates upside potential.

3) Implied forwards may not be realized, causing the yield curve to collapse lower

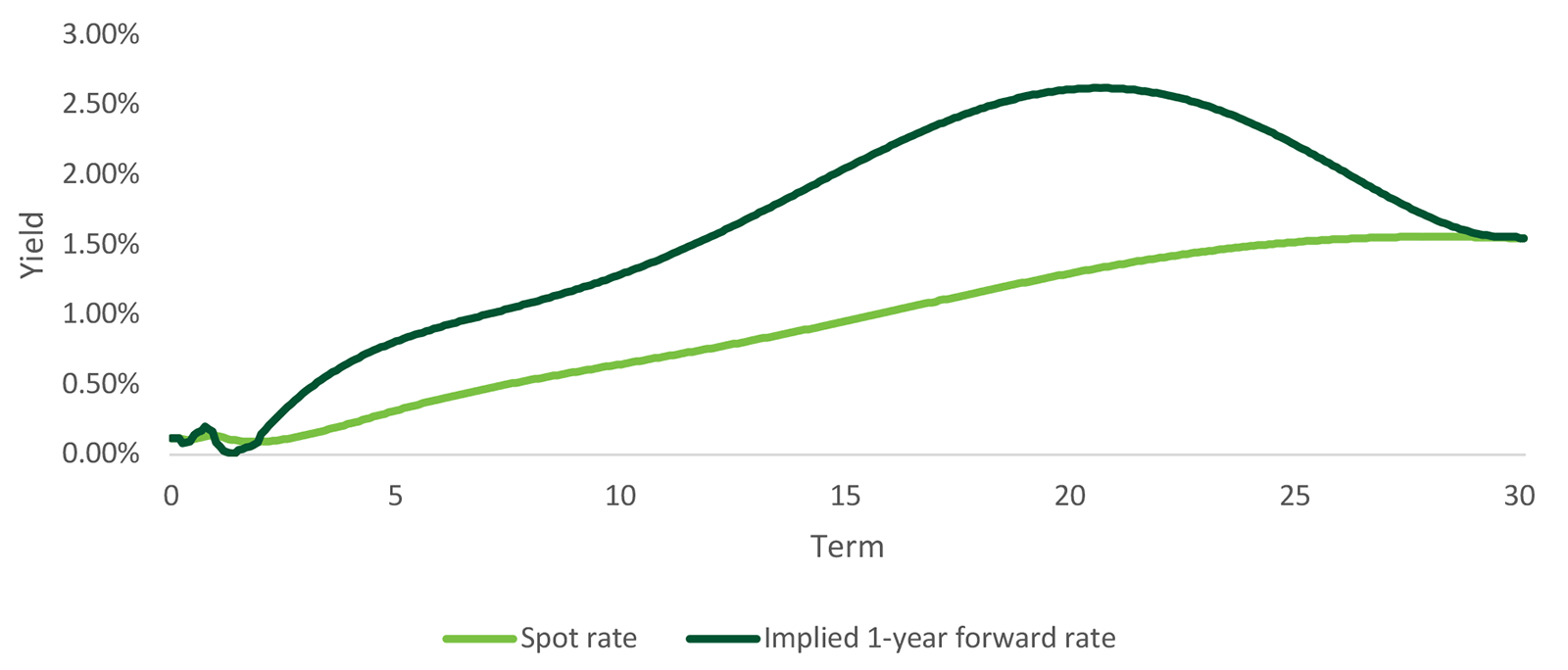

In order to benefit from rising rates, actual cash ‘spot’ rates need to rise faster than the implied ‘forward’ rates underlying the yield curve. In fact, if spot rates rise by less than implied forward rates – the plan’s dollar funded status deficit would actually increase.

Currently, the implied cash rates in future years show the 1-year rate rising from close to 0% today to 2.5% over 20 years (Figure 5).

Figure 5: Current spot vs forward curves5

To put this into context – the Fed Funds rates was last above 2.5% before the 2008 global financial crisis. Since then it has averaged less than 60bps. If anything, based on this there may be a risk that the yield curve is actually overstating the potential future path of interest rates and may even represent value.

Managing to your specific desired outcome

We have no way of knowing whether rates will rise or fall from here. However, armed with the right risk management tools you can adapt your approach to ensure that you have the right level of hedging and upside potential, but also sleep easy knowing that you also have the right level of downside protection in place to keep your problem ‘solvable’ if things go wrong.

1Insight calculations. Market conditions as of September 30, 2020. Baseline discount rate 2.60%. Plan statistics: Funded status 85%, Liability duration 15yrs, Benefit payments 6% p.a. of beginning assets. Plan is assumed to freeze in 2030 with Service Cost 1.5% of PBO in future years. Assumes the plan is 100% funded under accrued and future benefits at the end of the respective time horizon.Illustrative required excess return over discount rate to reach 100% funded; starting at 85% funded, 0.0% p.a. Service Cost accruals for 10 years only; assumes no minimum required contributions are planned. For illustrative purposes only. Does not represent any strategy, composite, or client account managed by Insight.

2For illustrative purposes only. Manager makes no assurances that potential benefits will be achieved. Derivatives are highly specialized instruments that require investment techniques and risk analysis different from those associated with equities and debt securities. Strategies may use both exchange-traded and over-the-counter derivatives, including, but not limited to, futures, forwards, swaps, options and contracts for differences. These instruments can be highly volatile and expose investors to a high risk of loss. There can be no guarantee or assurance that the use of derivatives will meet or assist in meeting the investment objectives of the strategy.

3Insight, hypothetical plan with starting duration of 12 years and discount rate in line with the Bank of America-Merrill Lynch AA curve +15bp. Assumes fixed cash flows.

4Insight, hypothetical plan with $10m in present value liabilities. Illustrative of average 2.5% initial discount rate and illustrative 14-year duration liabilities. Where model or simulated results are presented, they have many inherent limitations. model information does not represent actual trading and may not reflect the impact that material economic and market factors might have had on insight’s decision-making

5Insight, Bloomberg, September 2020

Any opinions expressed herein are Insight Investment’s own as of the date of publication and are subject to change without notice.