Institutional investors can enhance their ability to capitalize on the yield and diversification benefits of alternatives by focusing on the risks that drive returns in each specific segment of the alternatives universe. This approach allows investors to stitch together multi-asset portfolios in a more efficient, coherent way.

Executing this, however, is no simple task. If done incorrectly, investors risk negating some of the diversification benefits that make alternatives such valuable contributors to stronger, more resilient portfolios.

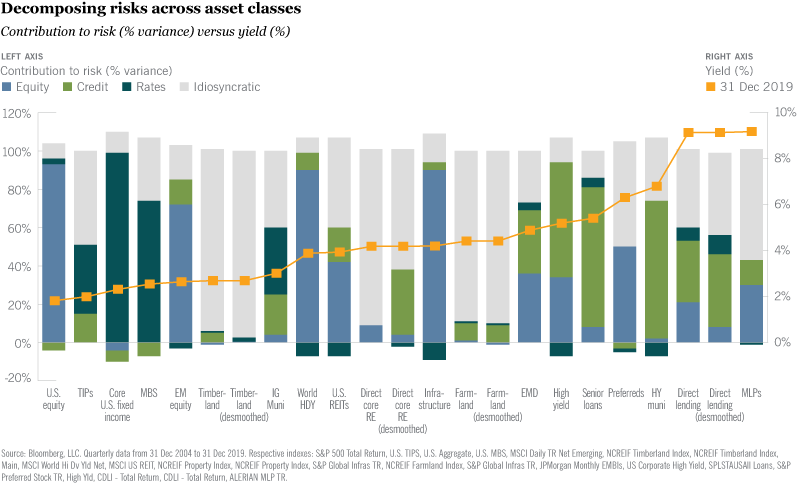

Know what risk factors drive return

Alternative asset classes such as private credit, real assets (farmland, timberland and private equity infrastructure investments) as well as non-traditional sectors of fixed income (preferred securities, emerging markets debt, high yield corporate debt and leveraged loans) present attractive income-generating potential.

Idiosyncratic risks play a vital role in driving returns in each of these asset classes — and these risks are what institutional investors should be trying to harness in an income-generating multi-asset portfolio. But it is important to note that each of these asset classes has significant exposure, in varying degrees, to the core, broad-based risk factors: equity, credit spread and rate duration.

As the chart below illustrates, idiosyncratic risks account for less than 60% of the contribution to total risk in most of the alternative asset classes included in the chart. With emerging markets debt, for example, equity risk accounts for 36% of the total risk and credit risk accounts for an additional 33%.

Preferreds are also an interesting case. Some investors consider them to be more like an equity instrument while others consider them to be more like fixed income. This debate is easily settled when viewed through a risk decomposition lens, which shows that equity risk and idiosyncratic risk account for the totality of risk for preferreds.

This isn’t to imply that emerging markets debt and infrastructure aren’t valuable diversifiers. Rather, it is to highlight that unless an investor decomposes the risk contributors, a portfolio could end up with significantly more exposure to equity, credit or rate risk than the investor bargained for.

Allocate to risk factors, not asset classes

Investors are compensated for owning risk, not asset classes. We believe that their portfolio construction processes should reflect this and we have developed a five-step approach to do just that:

- Decompose risk factors driving the performance of asset classes

- Analyze how the market is compensating those risk factors

- Determine which risks need to be owned to fulfill investment objectives and constraints

- Determine which asset classes and vehicles will achieve the desired risk exposures

- Monitor risk and asset class relationships and how the market is compensating risks

Three benefits of a risk-first approach

This framework puts risk at the heart of constructing multi-asset portfolios and delivers multiple benefits to investors. As already noted, it reduces the risk of overconcentration of risk factors in a portfolio, which could undermine the diversification benefits investors seek from alternatives.

It also encourages a more nimble approach to pursuing yield. The relationships among the risk factors and thus the relationships among the asset classes are constantly evolving — and the degree to which the market is compensating various risks is always changing. Predefined asset allocation constraints limit an investor’s ability to exploit these changes and manage risk.

The framework fosters a more nuanced approach to managing liquidity. Liquidity risk is just one of the idiosyncratic risks of an investment. But when using alternatives to generate income and cash flows needed to fund a set liability, liquidity becomes the idiosyncratic risk that institutions need to understand the best. Taking a risk-first approach to multi-asset portfolio construction frees an investor to take a more nuanced and sophisticated approach to managing liquidity risk — not just with alternatives, but across the entire portfolio.

Learn more about harnessing alternative sources of income

Download the paper on Nuveen.com for a deeper dive on our recommendations on risk factor-based portfolio construction, as well as our analysis of specific income-generating alternative asset classes.

We examine four asset classes that offer attractive income-generating potential and discuss the primary risks that drive returns in each: non-traditional sectors of fixed income, private credit, real assets and real estate. We also share our latest views on the opportunities and positioning considerations for each of these asset classes.

Endnotes

Sources

All market and economic data from Bloomberg, FactSet and Morningstar.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature.

Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance is no guarantee of future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

A word on risk

All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investing involves risk. Investments are also subject to political, currency and regulatory risks. These risks may be magnified in emerging markets. Diversification is a technique to help reduce risk. There is no guarantee that diversification will protect against a loss of income. Investing in municipal bonds involves risks such as interest rate risk, credit risk and market risk, including the possible loss of principal. The value of the portfolio will fluctuate based on the value of the underlying securities. There are special risks associated with investments in high yield bonds, hedging activities and the potential use of leverage. Portfolios that include lower rated municipal bonds, commonly referred to as “high yield” or “junk” bonds, which are considered to be speculative, the credit and investment risk is heightened for the portfolio. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC/CC/C and D are below-investment grade ratings. As an asset class, real assets are less developed, more illiquid, and less transparent compared to traditional asset classes. Investments will be subject to risks generally associated with the ownership of real estate-related assets and foreign investing, including changes in economic conditions, currency values, environmental risks, the cost of and ability to obtain insurance, and risks related to leasing of properties. Socially Responsible Investments are subject to Social Criteria Risk, namely the risk that because social criteria exclude securities of certain issuers for non-financial reasons, investors may forgo some market opportunities available to those that don’t use these criteria. Investors should be aware that alternative investments including private equity and private debt are speculative, subject to substantial risks including the risks associated with limited liquidity, the use of leverage, short sales and concentrated investments and may involve complex tax structures and investment strategies. Alternative investments may be illiquid, there may be no liquid secondary market or ready purchasers for such securities, they may not be required to provide periodic pricing or valuation information to investors, there may be delays in distributing tax information to investors, they are not subject to the same regulatory requirements as other types of pooled investment vehicles, and they may be subject to high fees and expenses, which will reduce profits. Alternative investments are not suitable for all investors and should not constitute an entire investment program. Investors may lose all or substantially all of the capital invested. The historical returns achieved by alternative asset vehicles is not a prediction of future performance or a guarantee of future results, and there can be no assurance that comparable returns will be achieved by any strategy.

Nuveen provides investment advisory services through its investment specialists.

GWP-1192253PF-Y0620P