David Wilson

Eight years of nearly uninterrupted economic growth and stock market gains have barely made a dent in the funded status of US corporate and public pension plans. We may now be approaching an inflection point: most analysts agree the current economic expansion is in its later stages, and the Federal Reserve has begun to unwind the extraordinary measures it took in the wake of the 2008 financial crisis to bolster the economy. Chief Investment Officer spoke recently with David Wilson, head of Nuveen Asset Management’s Institutional Solutions Group, to find out what the potential ramifications are for plan sponsors as the economic climate changes, and why corporate and public plans may need to respond differently.

Q: The current US economic expansion is getting old; it’s already the third-longest since 1854. What are some of the biggest challenges and

opportunities defined benefit plans will face when the economic cycle starts to turn?

David Wilson: Unfortunately, there will be more challenges than opportunities, in my view. The persistently low interest-rate environment is the biggest challenge corporate pension plans have faced since 2008 because it’s increased the value of their liabilities while simultaneously dampening future expected returns on fixed-income portfolios. We don’t see that changing for quite some time. Looking specifically at corporate pension plans, most still have large allocations to global equities, and when the economic cycle turns down, equity prices typically fall. Given that corporate plans are already underfunded—the average plan had an 82% funded ratio at the end of September—this could present another major challenge. Public pension plans are not as impacted by interest rates as corporate plans, at least on the liability side, since their liability discount rate is fairly static. But on the asset side, many plans have reduced their fixed-income allocations due to the low rate environment and fears that we will enter into a rising rate environment. They face even greater challenges with respect to a future downturn in equity prices.

Q: Why would an equity market downturn hit public plans harder than corporate plans?

Wilson: Public plans typically invest about 75% of their assets in return-seeking strategies like equities and alternatives, which is a good bit more than the average corporate plan. So, they’re taking on more investment risk. They also are far more underfunded. According to a recent survey, the average public plan had a 71% funded ratio in 2016 using a liability discount rate of 7.5%. Compare that to the average corporate plan that’s 82% funded with about a 4% discount rate, and you can see that public plans are in a very different economic situation. For both types of plans, though, the headline message is that with potentially more challenges than opportunities on the horizon, it is vital that they protect their investment portfolios using sophisticated risk-management techniques.

Q: Let’s focus on corporate plans for a moment. A lot of them have been trying to de-risk for years, primarily through some form of liability-driven investing. Why hasn’t this led to improved funding ratios?

Wilson: Beginning in 2008, long-term interest rates started going lower and then stayed low—historically low, actually— so many plans weren’t able to make progress on their de-risking glide path. They weren’t able to hit their glide-path triggers because falling rates boosted the value of their liability. Then, in 2014, mortality tables were updated, which caused their liability to rise again, and their funded ratio just continued to struggle, despite generally increased contributions and strong investment returns.

Q: Do you see better results from liability-driven investing moving forward?

Wilson: I think corporate plan sponsors will generally be disappointed with the effectiveness of most LDI strategies as plans achieve higher funding ratios and seek precision in their asset/liability match. The primary reason is that the benchmarks used in traditional de-risking strategies, namely the Barclays Long Credit Index and the Barclays Long Government/Credit Index, simply were not created for pension plans. They are subsets of the Barclays Aggregate index, which represents bonds outstanding, which in turn means these indexes really represent issuance patterns, not a pension plan’s liability. In the case of the Barclays Long Credit Index, for example, over 49% of the index is made up of BBB-rated securities. In the case of the Barclays Long Government/Credit Index, it’s about 29%. The latter index also has a substantial amount of Treasury securities. By contrast, pension liabilities are generally discounted, for funding purposes, using an index of A-rated to AAA-rated bonds and a discount curve derived from them. The upshot is that traditional market-based benchmarks have a lot of tracking error against pension discount curves—around 6% according to our research.

Q: How has asset/liability tracking error impacted pension plans overall?

Wilson: It’s been a significant issue, especially given that funded ratios remain so low for most corporate plans. Because of low funded ratios, many plan sponsors hold a certain amount of return-seeking assets to gain ground on their unfunded liability. As a result, even after all the talk and effort put into de-risking, the average asset allocation for a corporate pension plan today is still close to 60/40, meaning 60% return-seeking assets and 40% fixed-income or liability-hedging assets. The risk a 60/40 portfolio presents on an asset/liability basis is quite substantial, especially during adverse market conditions. For example, in 2006, when markets were booming and volatility was low, a 60/40 portfolio had approximately a 5% annualized tracking error against a typical pension liability, which isn’t so bad. But in 2008, which was obviously an extraordinarily difficult year, that tracking error increased to 45% annualized. The last thing you want to happen while you’re pumping money into your pension plan is to have this tracking error further derail your de-risking strategy. Merely extending the duration of your fixed-income allocation to better match a portion of your liability’s duration, which is all that many plan sponsors do, doesn’t really have a significant impact on overall plan risk. You also have to address the return-seeking side of the portfolio.

Q: What tools can corporate plans use to manage risk?

Wilson: There are a wide variety of tools available to plan sponsors. One we like, for plans that have large equity allocations, is a managed volatility approach in which we identify the exact amount of risk, from a volatility perspective, that the plan is willing to take, and then manage to that target using a futures-based overlay. As an example, let’s say the plan has exposure to a large-cap equity strategy and needs to maintain a growth portfolio because the plan is underfunded—but can’t withstand the substantial volatility risk that the asset class presents. We might set an annualized volatility target of 12% for that growth portfolio, and create a volatility band around that from, say, 10% to 14%. When we forecast volatility to be above our 14% threshold, we’ll sell equity futures and bring the market exposure down and volatility back within the range.

Q: Once a plan sponsor is ready to fully de-risk, how can they minimize tracking error? Can’t derivatives help?

Wilson: Derivatives are anathema to many plan sponsors, especially smaller ones. But there is a simpler way. At Nuveen, we worked in collaboration with Wilshire Analytics to develop a family of four indexes, introduced just last year, designed specifically for corporate pension plans. The Nuveen Wilshire Pension Investment Indexes seek to provide an effective de-risking solution— customized for all plan sizes— with a simple implementation. They also serve as both an asset benchmark and a liability benchmark. They enable a plan sponsor to judge whether the bond manager is adding value against the benchmark and whether the LDI program is effective.

Q: How do these new indexes work, and how do they contrast with traditional pension plan benchmarks?

Wilson: The indexes cover the corporate universe of A-rated bonds and better, which means they closely match the credit quality of pension discount curves. They are distinguished from one another by their maturity range (e.g. five to 10 years, 10 to 20 years, and 20 to 30 years), because if you think about a pension liability, it’s a series of cash flows that can be bucketed very similarly to the way we bucketed our indexes. We also developed an ultra-long STRIPS index solely for extending duration when needed against a plan’s long-dated liabilities—without needing derivatives. Also, one of the things we were trying to solve for during the development process was allowing smaller plans to have access to the same level of customization that’s long been available to their larger peers, using products they know and can understand. So, earlier this year, we launched a series of collective investment trusts managed against each of these indexes, with a $1 million minimum account size. This means even very small corporate pension plans can get the same level of customization and precision available to much larger plans.

Q: Let’s turn to public pension plans. How are their challenges different from those facing corporate plans?

Wilson: Public plans and corporate plans are fundamentally the same at their core. It’s the differences in their accounting and regulatory treatment that make them different from an investment strategy perspective. Corporate plans value their liabilities using a market-based yield curve, which means their liabilities carry duration and credit spread premium risks that need to be managed. Public plans, generally speaking, have a more static, non-market-based discount rate—which currently averages about 7.5%—which means their liability does not have any duration or credit spread risk.

Beyond these distinctions, public plans are even more underfunded, and that presents some unique challenges for them. To be fair, many public plan sponsors have recognized this and have done the best they can, within the scope of their budgets, to increase their contributions to their plans. But now they’re facing new demographic challenges, too.

Their ratio of active employees to retirees has been declining steadily for years, to the extent that many plans now face ratios approaching or below one, meaning there are more retirees in their plans than there are active employees. The consequence, from an investing perspective, is a shortening investment time horizon. We all tend to think of pension plans as these perpetual entities, as the ultimate long-term investors. The reality is they aren’t in many cases, because with more and more people retiring and drawing benefits, the size of their annual benefit payments is steadily increasing—and will continue to do so for the next 20 to 25 years.

Q: How is this shrinking active-to-retiree ratio impacting investment strategy at public plans?

Wilson: It’s limiting their ability to take on risk. I use this simple example to illustrate the problem. If you’re sending your child to college next year, and you have the cash on hand but want to invest it, are you going to buy stocks or a one-year bond? Chances are you’re going to buy the bond, because your investment time horizon is too short to risk losing that tuition payment. It’s no different for the pension plan that has benefit payments that are coming up this year, next year and every year thereafter and are increasing along the way. If we have a correction in the equity markets, or even worse, a recession, and the plan has a large return-seeking portfolio—at the same time it has increasing benefit payments and a shortening investment time horizon—it could be facing a real crisis.

Q: So how can public plans adjust their investment strategy—knowing they’ve still got a big unfunded liability that could desperately benefit from return-seeking assets?

Wilson: One approach we’ve developed is called demographic-based investing, in which we seek to align the risk of the investment portfolio with the obligation. We do that by first breaking out the plan’s liability into segments—active employees, retirees, terminated vested employees—and thinking about the characteristics of each. For active employees, the benefits have not been calculated yet because employees are still accruing them. They may retire next year, they may retire in 50 years. Generally speaking, the tenor of that liability is long, and the ultimate size of the liability might be tied to inflation or wage growth. If you wanted to precisely match assets to it, you couldn’t; it’s too long, and there are too many uncertainties. But the characteristics of that liability align very well with growth-related assets, such as equities and certain alternatives, so we recommend allocating to those strategies against this segment of the liability.

If you look at the retiree segment, by contrast, the benefits have already been calculated and have a shorter tenor. The only real variability is how long people live. This segment of the liability can be addressed from a matching perspective, but we don’t try to duration-match it, we cash flow-match it—because, as I mentioned earlier, there is no duration risk associated with a public plan liability.

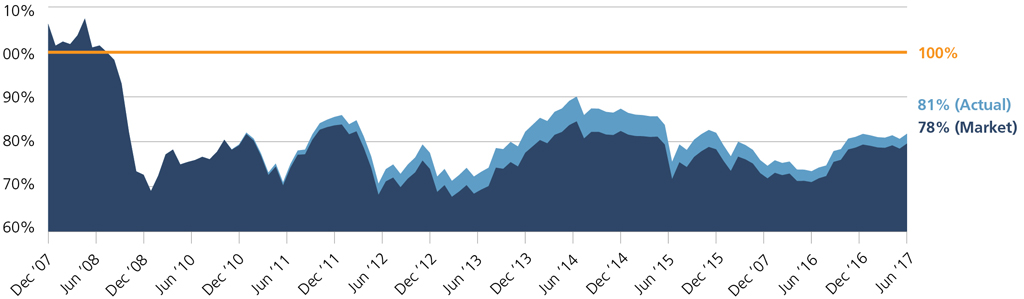

US Corporate Pension Funded Ratios Have Remained Low Since 2008 Credit Crisis

Nuveen Asset Management’s Funded Ratio Tracker shows the mont-to-month funded ratio changes of a typical US corporate defined benefit pension plan. Nuveen tracks two separate funded ratios—an “Actual” ratio, which accounts for non-market items such as contributions, service costs and benefit payments, and a “Market” ratio, which focuses on the funded ratio changes due only to interest rates, spreads, and asset returns. As shown in the graphic below, both ratios have remained well below 100% since the 2008 credit crisis, despite a strong performance by the equity markets over the past nine years.

Sample Demographic-Based Investing Asset Allocation

The chart below shows the allocation to fixed-income and diversified growth assets for each annual pension payment for a hypothetical defined benefit plan, using Nuveen’s demographic-based approach to investing.

In this example, 26% of the pension payment obligation is matched with fixed-income cash flows.

Q: Is this a one-size-fits-all solution?

Wilson: No. This approach needs to be customized for each individual plan. It starts with an understanding of the plan’s specific obligation and then seeks to reposition the fixed-income allocation of the plan’s assets from a traditional total-return approach to a cash-match approach. It’s also responsive to changes in the plan. As benefit payments increase, you can match more of your liability. As your funded ratio increases, you can match more of your liability. You can customize the match to get to your desired duration. You also can customize your investment portfolio to your desired credit risk. The net result is that this approach reduces investment risk because you’re no longer concerned about duration risk, your objective is to match cash flows. And by the way, in some cases you can enhance the yield of the fixed-income portfolio along the way, too.

Q: In effect, you’re eliminating, or at least minimizing, the threat pension plans face of having to sell return-seeking assets simply to make benefit payments, right?

Wilson: Exactly. If your plan is underfunded and you’re making benefit payments, every time you sell an asset to meet a benefit payment your funded ratio ticks down. A simple example is if you have $80 of assets and $100 of liabilities, and you make a $10 payment, your assets are now $70 and your liability is $90. Just by making that payment, you went from an 80% funded ratio to a 77% funded ratio. If you had that situation combined with a market downturn, you could have a dramatic acceleration of that downward spiral in your funded ratio—something we refer to as the Black Hole scenario. What demographic-based investing does is mitigate the need to sell return-seeking assets to meet plan payments. Instead, your bond investments are maturing alongside your benefit payments. Another key benefit is that this approach extends the time horizon of your return-seeking assets so they have more opportunity to play out over multiple markets cycles.

Q: So you’re not expecting interest rates to go up? You alluded to this earlier.

Wilson: It’s worth noting that we’ve all been wrong about the impending rate rise for the past eight or so years. Now we’re in a later stage of a very long economic recovery and expansion, and there’s no certainty that rates will rise and save corporate defined benefit plans, particularly if economic growth begins to slow. Also, it is important to point out that long-term interest rates are what really matter to corporate plans because their liabilities are long-term. For example, if the Fed increases its federal funds rate target, that doesn’t necessarily impact the level of longer-term rates and thus may not matter to the plan.

Q: We’ve covered a lot of ground. What’s the most important thing you want plan sponsors to take away from this discussion?

Wilson: I’ve been encouraging all of my clients, and all of the prospects I meet, to focus on managing their asset/liability risk—the volatility of their funded ratio—rather than continue to wait for interest rates to go up and solve all their problems.