Author: Rene Martel Global Head of Pension Solutions

Hibernation strategies, a lower-cost alternative to pension risk transfers, may lead to better outcomes for plan sponsors in the medium term – and even put the plan sponsor in a better position for a more successful pension risk transfer in the future.

A common argument in support of PRTs revolves around the idea of reducing Pension Benefit Guarantee Corporation (PBGC) premiums. The PBGC levies premiums on single- employer plans on two fronts – a “per head” premium (the fixed rate premium) and, for underfunded plans, a variable rate premium (VRP) based on the percentage of a plan’s unfunded liability.

There is some merit to the idea that PRTs can help plan sponsors reduce their participant count and, as a result, also reduce their fixed rate PBGC premiums. The fly in the ointment, however, is that while premiums are reduced, they may not fall as much as if the sponsor were to choose a strategy other than PRT.

PARTIAL PENSION RISK TRANSFERS: TWO SCENARIOS

Scenario 1

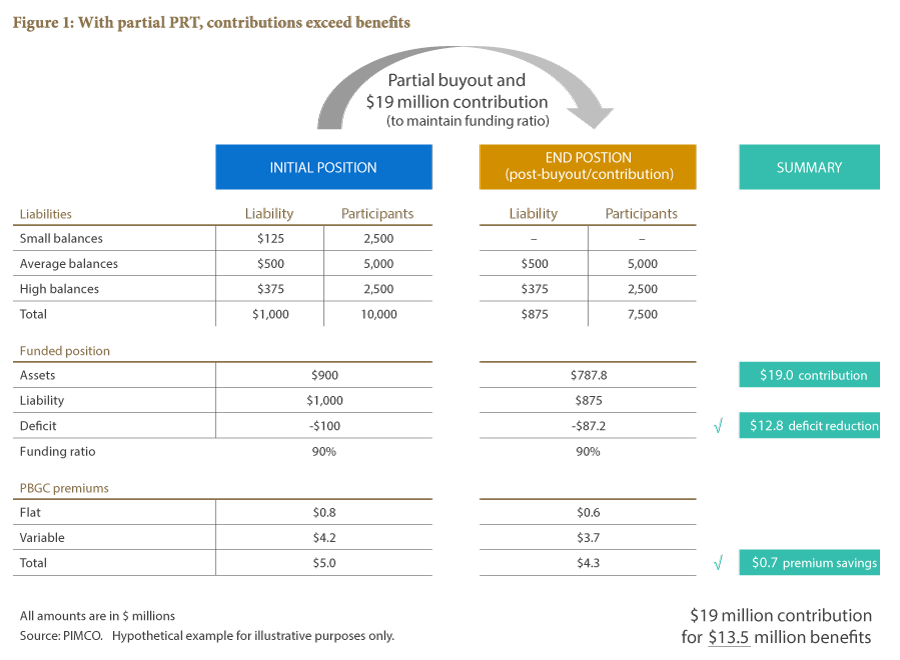

Figure 1 shows a hypothetical plan with 10,000 participants and a 90% funded ratio ($900 million in assets and $1.0 billion in liabilities). The plan sponsor is considering transferring the liability associated with small balances to an insurance company in an effort to reduce its liability value, participant count and PBGC premiums. For example, in exchange for providing annuity payments for $125 million of liabilities, the insurer will require a single premium that exceeds the value of the liability transferred, as the insurance company builds in conservatism margins, capital costs, profit loadings, etc. Assuming a 5% premium over the value of the projected benefit obligation (PBO) liability, our hypothetical plan sponsor would transfer $131.25 million of assets to annuitize $125 million of liabilities.

The funding ratio would fall given the plan’s initially underfunded position and because a larger amount of assets than liabilities is transferred. Further, in fairness to participants who remain in the plan after the transaction, plan sponsors typically make a contribution to restore the funding ratio to its pre-transaction level. In our example, the plan would need to contribute $19 million to maintain the funding ratio at its pre-transaction level.

When all is said and done, it may appear as if the plan sponsor achieved its objective owing to a meaningful reduction in participant count (25% or 2,500 individuals) and liability value (a 12.5% decline, or $125 million).

But how do we assess whether this constitutes a sufficient reward in light of costs and resources commitment incurred by the sponsor?

One could begin an assessment by quantifying the benefit in dollar terms and comparing this to the “costs” incurred. In our example, the plan sponsor achieved a $12.8 million reduction in its deficit and a $0.7 million reduction in its annual PBGC premium. Overall, the plan gets advantages worth $13.5 million in exchange for a $19 million contribution to the plan. (Our intent, of course, is not to compare these two numbers because the $19 million outlay is a one-time cost while some elements of the $13.5 million advantage will be recurring).

The question remains, however: Would the sponsor achieve the maximum possible benefit for its $19 million commitment?

Click here to read the full article

All investments contain risk and may lose value. The objectives and funding needs for defined benefit plans will vary and a liability driven investing (LDI) strategy should not be considered a complete investment program. The examples provided are not intended to be a recommendation for any particular defined benefit plan’s use, and should not be relied upon as such.

Hypothetical and simulated examples have many inherent limitations and are generally prepared with the benefit of hindsight. There are frequently sharp differences between simulated results and the actual results. There are numerous factors related to the markets in general or the implementation of any specific investment strategy, which cannot be fully accounted for in the preparation of simulated results and all of which can adversely affect actual results. No guarantee is being made that the stated results will be achieved.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve. No representation is being made that these scenarios are likely to occur or that any portfolio is likely to achieve results similar to those shown. The scenarios do not represent all possible outcomes and the analysis does not take into account all aspects of risk.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2019, PIMCO.

pimco.com

blog.pimco.com