What Are Minicycles?

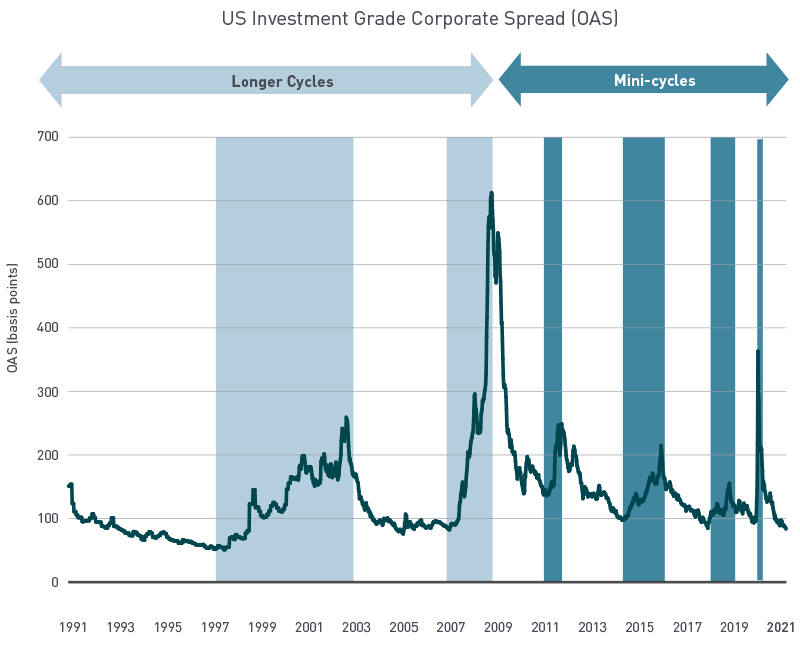

Before the global financial crisis (GFC), credit cycles typically lasted between five to seven years (Exhibit 1). However, since the GFC, more frequent periods of sharp spread widening followed by spread compression have occurred—what we refer to as minicycles. With these shortened cycles, spreads tighten and widen within only a couple of years. While the catalyst in each minicycle has been different, the underlying conditions that allow for this volatility in spreads have been the same.

Exhibit 1: Credit Spread Volatility Has Risen Post-GFC

Shaded areas represent periods of significant spread widening. Source: Bloomberg. Weekly data from 1 March 1991 through 28 May 2021. US Investment Grade Corporate = Bloomberg Barclays US Aggregate Corporate Index.

Understanding Credit Spreads

A credit spread is the difference in yield between a risk-free bond such as a US Treasury bond and another bond with the same maturity. Credit spreads often reflect market sentiment. In general, spreads are wide when investors are risk averse and demand higher yield as compensation, and narrow when investors are willing to take on risk and receive lower yield as compensation.

New Market Dynamics Fueling Minicycles

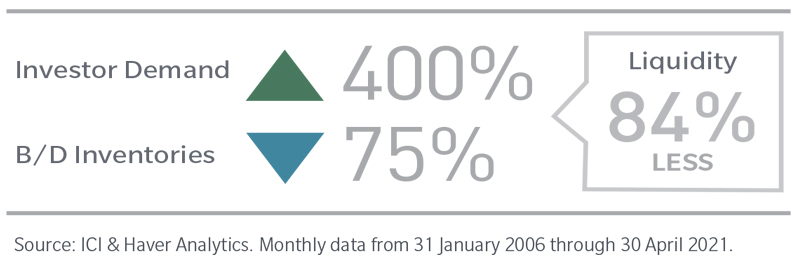

Shrinking liquidity: The lack of liquidity since the GFC has been the biggest factor contributing to these minicycles. The regulatory changes enacted in the aftermath of the GFC all but ended broker/dealer (B/D) proprietary trading, an important source of liquidity. Dealer inventories dropped from about $100 billion pre-GFC to about $25 billion today.

Growing demand: While liquidity was declining, the market was rapidly growing. Investor demand for US corporate bond mutual funds and exchange-traded funds (ETFs) has almost quadrupled since the financial crisis.

Result: The liquidity “pipe” has shrunk to a sixteenth of its size before the GFC. Moreover, liquidity is further exacerbated by an investor base that often moves in the same direction—buying when the market goes up and selling when the market goes down—and dealers that reduce their risk in sync with the herd. This is a recipe for dislocation and volatility in the markets and minicycles. We don’t expect this market dynamic to change in the near term.

Opportunities for Active Managers

While spread volatility has its challenges, it also creates opportunities for experienced active managers. This involves the willingness to give up higher current yield for a period to be able to potentially add more alpha over the course of the minicycle by recognizing critical points in the minicycle and acting tactically in both sector allocation and security selection. This means selling when spreads are at the tighter end of their historical range and buying at attractive/cheap prices when markets decline and spreads widen, providing liquidity when others are selling.

Although this means giving up higher current yield for a period, in our view, the potential to generate future returns through price appreciation when markets recover outweighs the lost carry. The key to capturing return potential during these short-lived minicycles is a disciplined valuation process: selling early when spreads are tight so you can provide liquidity (i.e., buy) during dislocations when spreads widen and valuations are cheap. To put it succinctly, you need to be early to be right.

Discipline, Research and Risk Management Are Key

We believe capturing opportunities through minicycles takes an active investment process, deep research, and a strong focus on risk management. Unlike passive managers who buy and hold, or active managers that chase gains, our investment teams analyze bonds, global economies, and markets to take a view on credit cycles and seek to take advantage of opportunities during periods of market volatility. This means reducing risk to be able to increase it later when the markets are in turmoil. This demands confidence in your research and the ability to stay disciplined on valuation and to be early, especially in selling.

The views expressed are those of the author(s) and are subject to change at any time. These views are for informational purposes only and should not be relied upon as a recommendation to purchase any security or as a solicitation or investment advice from the Advisor.

Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material or guarantees the accuracy or completeness of any information herein or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Index data source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

Unless otherwise indicated, logos and product and service names are trademarks of MFS® and its affiliates and may be registered in certain countries.

Distributed by: U.S. – MFS Institutional Advisors, Inc. (“MFSI”), MFS Investment Management and MFS Fund Distributors, Inc.; Latin America – MFS International Ltd.; Canada – MFS Investment Management Canada Limited. No securities commission or similar regulatory authority in Canada has reviewed this communication; Note to UK and Switzerland readers: Issued in the UK and Switzerland by MFS International (U.K.) Limited (“MIL UK”), a private limited company registered in England and Wales with the company number 03062718, and authorised and regulated in the conduct of investment business by the UK Financial Conduct Authority. MIL UK, an indirect subsidiary of MFS®, has its registered office at One Carter Lane, London, EC4V 5ER. Note to Europe (ex UK and Switzerland) readers: Issued in Europe by MFS Investment Management (Lux) S.à r.l. (MFS Lux) – authorized under Luxembourg law as a management company for Funds domiciled in Luxembourg and which both provide products and investment services to institutional investors and is registered office is at S.a r.l. 4 Rue Albert Borschette, Luxembourg L-1246. Tel: 352 2826 12800. This material shall not be circulated or distributed to any person other than to professional investors (as permitted by local regulations) and should not be relied upon or distributed to persons where such reliance or distribution would be contrary to local regulation; Singapore – MFS International Singapore Pte. Ltd. (CRN 201228809M); Australia/New Zealand – MFS International Australia Pty Ltd (“MFS Australia”) (ABN 68 607 579 537) holds an Australian financial services licence number 485343. MFS Australia is regulated by the Australian Securities and Investments Commission.; Hong Kong – MFS International (Hong Kong) Limited (“MIL HK”), a private limited company licensed and regulated by the Hong Kong Securities and Futures Commission (the “SFC”). MIL HK is approved to engage in dealing in securities and asset management regulated activities and may provide certain investment services to “professional investors” as defined in the Securities and Futures Ordinance (“SFO”).; For Professional Investors in China – MFS Financial Management Consulting (Shanghai) Co., Ltd. 2801-12, 28th Floor, 100 Century Avenue, Shanghai World Financial Center, Shanghai Pilot Free Trade Zone, 200120, China, a Chinese limited liability company regulated to provide financial management consulting services.; Japan – MFS Investment Management K.K., is registered as a Financial Instruments Business Operator, Kanto Local Finance Bureau (FIBO) No.312, a member of the Investment Trust Association, Japan and the Japan Investment Advisers Association. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks, including market fluctuation and investors may lose the principal amount invested. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

FOR INVESTMENT PROFESSIONAL AND INSTITUTIONAL USE ONLY. Should not be shown, quoted, or distributed to the public.

MFSP-FLY-901700-7/21 48922.1